EMBRACER: Compounder by Nature!

Youtube (summary video):

My Twitter account: https://twitter.com/MarketOriginal

PDF file of this article: https://drive.google.com/drive/folders/1x9tdjWRz5hyUiE2RCVGyPtupMQsocDgJ?usp=sharing

Spanish version of this article: https://www.rankia.com/blog/cazando-valor/5391731-embracer-compounder-natural

DISCLAIMER

All investment strategies involve risk of loss. By no means this is a customized service: each investor must assess whether this investment idea fits their personal financial circumstances. Nothing contained in this text should be construed as investment advice. Any reference to an investment's past or potential performance is not and should not be considered a recommendation or guarantee of any specific outcome or profit.

1. Highlights of the Company

It is a company in the technology sector, specifically in the video game industry. Without a doubt, it is a highly competitive sector with formidable and bigger rivals, however, it has very favorable tailwinds for the future.

It is a company that uses M&A as a long-term growth strategy, which somewhat dilutes the shareholder but contributes to overwhelming growth.

At the head we have a management that thinks in the long term and has experience in its M&A strategy, which has been executing successfully for several years.

Here we have some concepts that may be useful when studying EMBRAC:

-Game Developers: is the company that develops video games (works with programmers, cartoonists, animators, etc.).

-Game Publisher (see here): The Game Publisher advances money to the Game Developer to develop the game under an agreement. They usually supervise the game to verify that what was agreed is developed and then they usually help with marketing, national and foreign sales, the translation of the video game, etc.

-Video game rating must be seen here.

2. Company Overview

Embracer Group has a long history, which can be viewed here. Broadly speaking, Lars Wingefors is the founder and current CEO of EMBRAC. From a very young age he had entrepreneurial initiatives and suffered a very strong economic setback at the beginning of his career: in 2000, at the age of 22, he sold his company to a British startup for GBP 8M. What was the problem? The payment he received was not in cash, but in stock, and the deal was made in the same week that the dotcom bubble began to implode. In 2004, having overcome the impasse, Lars founded Game Outlet Europe (GOE), and in 2007 he started the video game publisher brand Nordic Games within GOE. In 2011, Nordic Games Holding acquires the assets of the insolvent JoWooD Entertainment and its subsidiaries: it is the beginning of the acquisition strategy. In 2014, Nordic Games acquires the American company THQ: THQ Nordic AB is born. In 2016 they are listed on the public markets through Nasdaq First North Stockholm and investors have the opportunity to be part of this success story, the acquisitions continue. In 2019, to avoid confusion between the subsidiary and the parent holding company, the latter changes its name to Embracer Group.

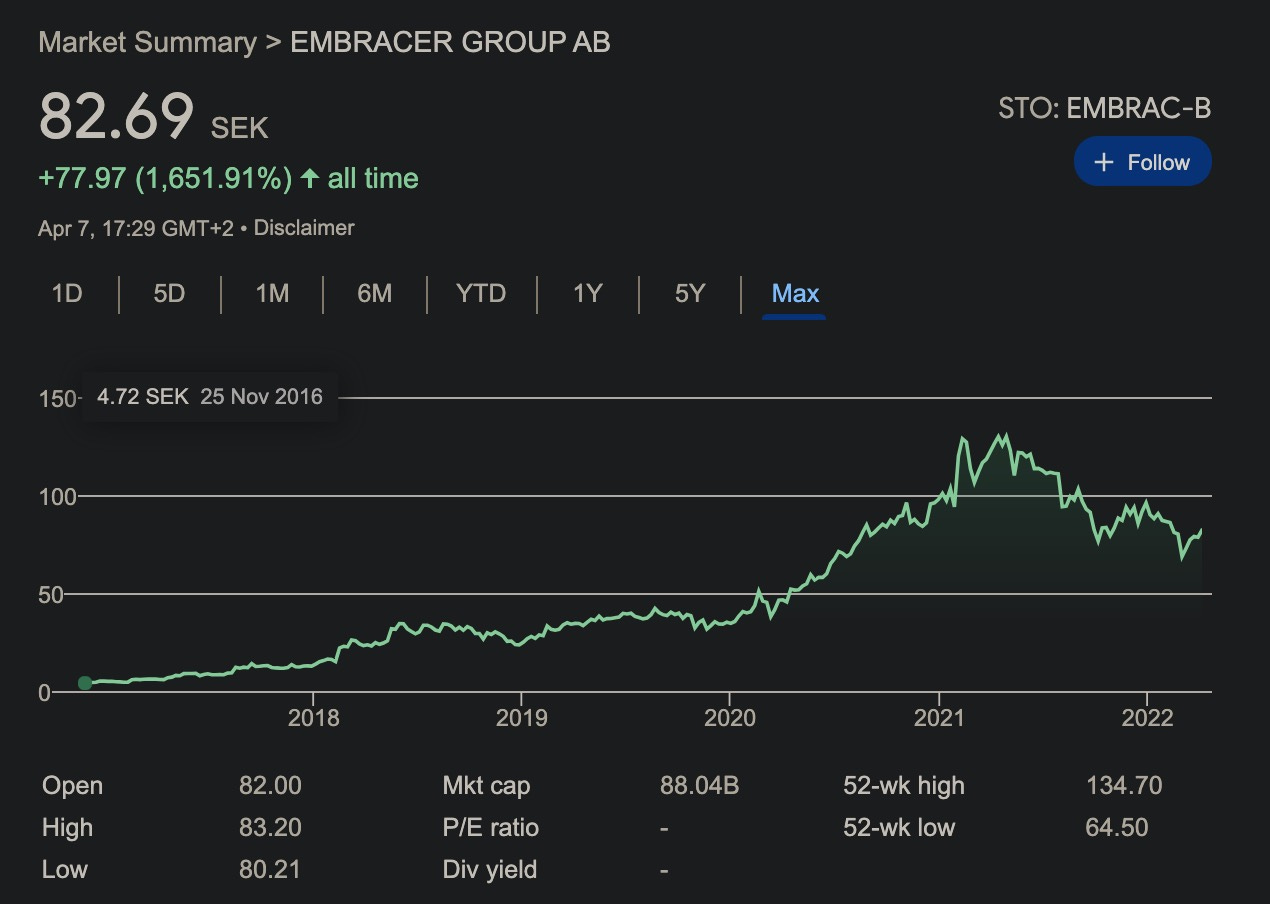

Since its listing, shares of this company have been a full-fledged multibagger, going from around SEK 5 to over SEK 100, before the general market decline since the end of last year.

An important feature is that EMBRAC operates, as has already been said, as a holding company that protects its subsidiaries like an umbrella and provides a series of benefits, which we will see later.

3. Business Model

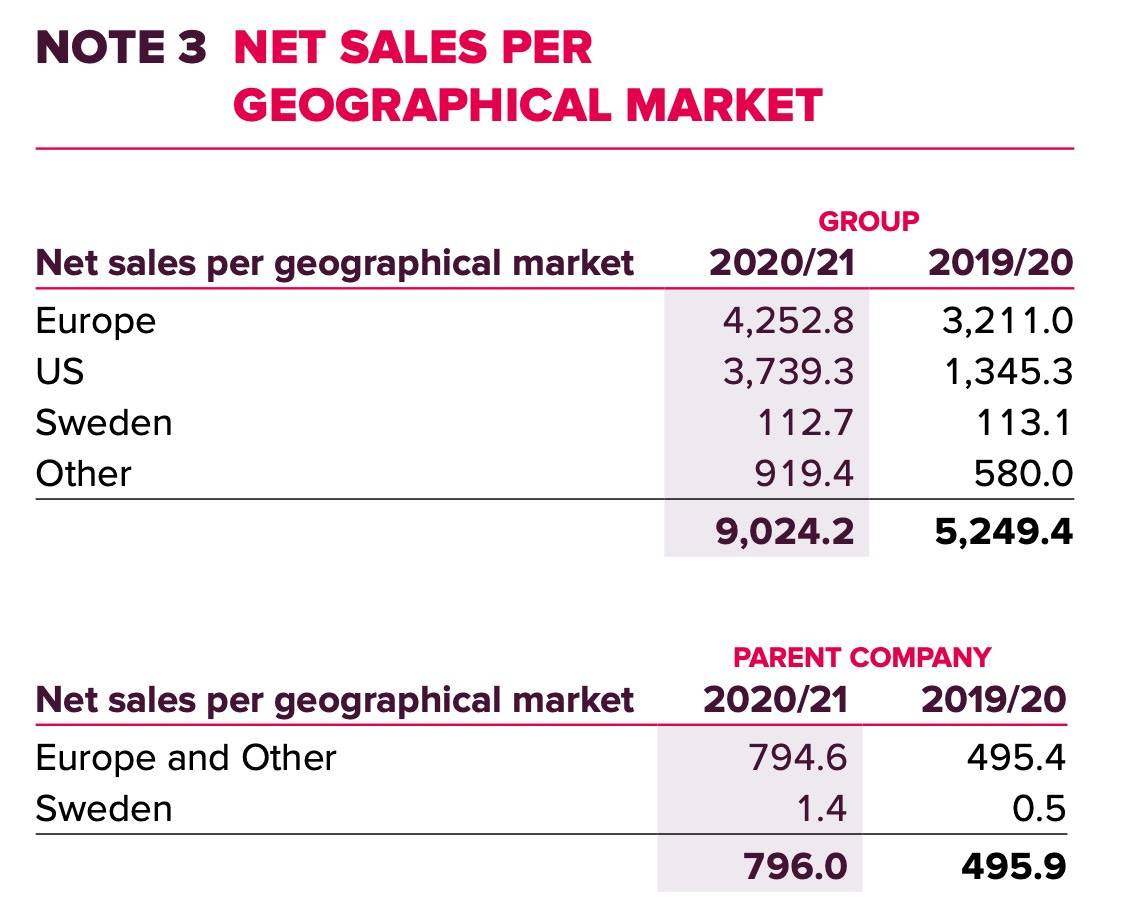

It is a business whose sources of income are diversified between different regions, the most important being Europe and the USA.

It presents its business lines as "Business Area", subdivided into "Operating Units", and it’s divided as follows (according to the most recent quarterly report Q3 2021/2022):

1. Business Area: Games

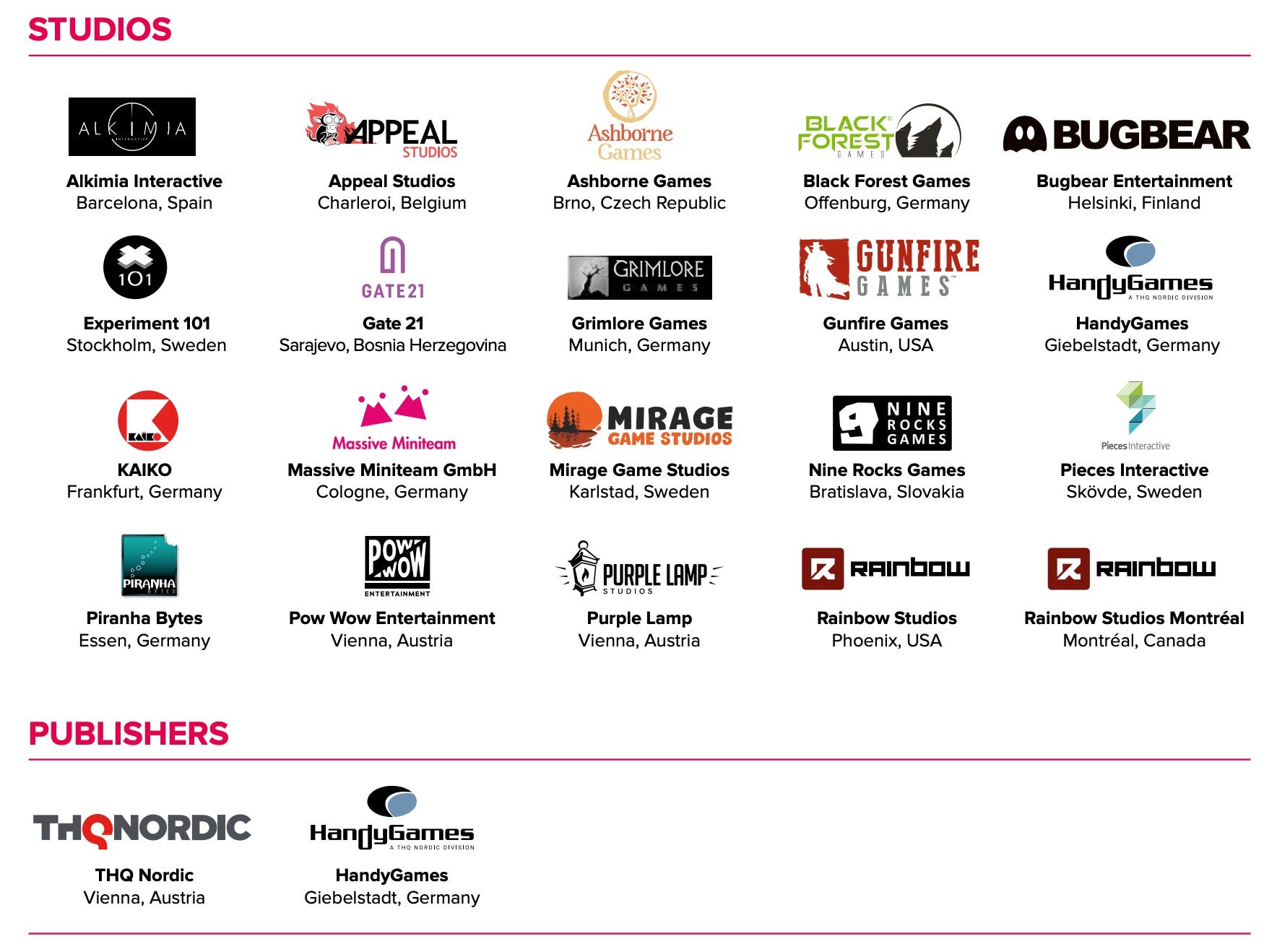

1.1. THQ Nordic (Austria): “THQ Nordic, based in Vienna, Austria, with subsidiaries in Europe, Japan and North America, is a global video game publisher and developer. THQ Nordic represents a core approach of doing much more than owning a highly competitive portfolio of IPs. It cherishes them with the very best development resources to expand to the level of experience that communities and fans expect and deserve”.

1.2. Koch Media (Germany): “The parent company is based in Höfen, Austria with operational publishing headquarters in Munich, Germany. Koch Media owns studios and offices in 15 countries around the world. It runs three distribution centers serving the European market, in the UK, Austria and Spain, and an external manufacturing and logistics partnership in Tennessee. Physical publishing in the US is mainly via partners such as Amazon, Walmart and GameStop. The strong market position of Koch Media as Partner Publisher is largely due to its expertise and experience to support the marketing of third-party publishing clients, managing the manufacturing and distribution of physical goods, inventory levels and offering reach into retail outlets. Although digital distribution has an ever-increasing portion of the global console and PC market’s sales, physical distribution still represents an important part of the total revenue”.

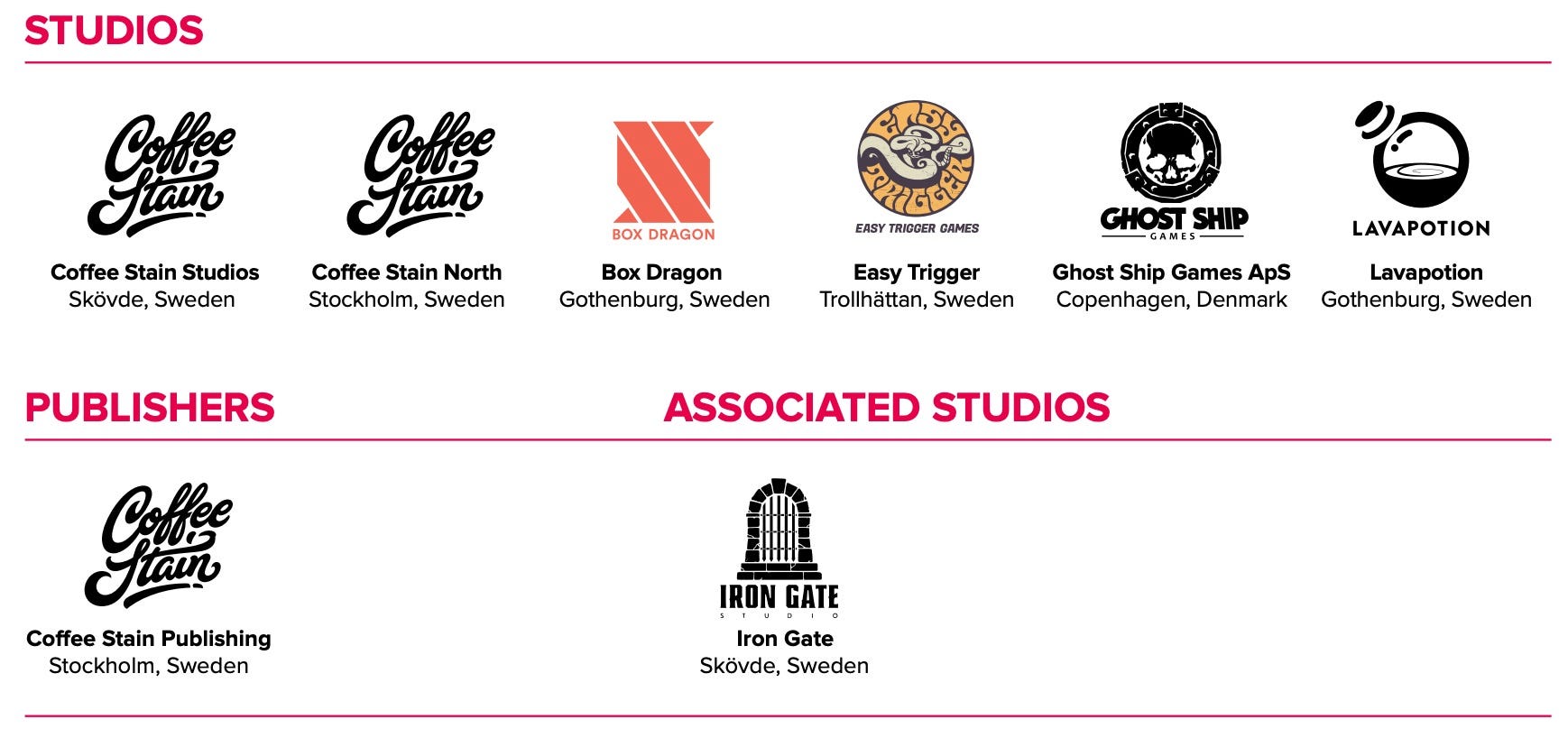

1.3. Coffee Stain (Sweden): “Coffee Stain is a world leading indie game developer and publisher, and its highly competent team create and publish great games. Particular s trengths in creating new products include its focus on digital sales, retention, cross platform and multiplayer. The Coffee Stain Group has been under the Embracer umbrella since November 2018, and holds four fully owned internal studios”.

1.4. Amplifier Game Invest (Sweden): “Amplifier Game Invest, acquired in August 2019, is becoming an important vehicle for our investments in new IP-development and teams. The business model is based on a partnership model designed to attract top talents through incentives and commercial support from the Group, while leaving them full creative integrity”.

1.5. Saber Interactive (USA): “Saber Interactive, founded in 2001, is an independent developer and publisher of high-quality video games for PC, consoles and mobile platforms. Saber is renowned for its strong technology knowledge and cost-efficient development. Saber also offers a unique platform for expansion in Russia and Eastern Europe. Embracer Group completed the acquisition of Saber Interactive on April 1, 2020”.

1.6. DECA Games (Germany): “DECA Games is an ecosystem of mobile publishers and developers with an expertise in live operations of Free-to-Play games. DECA started as an asset care business acquiring other developers’ games and IP and has evolved to add development studios and publishers since joining Embracer. Its business has highly complementary operations to Embracer Group’s existing and fast-growing business within PC/console game development and publishing. DECA Games was Announced as the sixth operative group within Embracer Group on acquisition, August 13, 2020”.

1.7. Easybrain (Cyprus): “On February 3, 2021, Embracer Group entered into an agreement to merge with Cyprus-based Easybrain Group Limited - a leading mobile games developer with a core focus on puzzle and logic game titles. By unlocking the potential of every team member, Easybrain strives to develop the best products on the market. Its' titles have more than 900 million installs to date and up to 12 million daily active users across 15 live games. Easybrain is announced Embracer's eighth operating group”.

1.8. Gearbox Entertainment (USA): “On February 3, 2021, Embracer Group AB entered into a merger agreement with US-based Gearbox Entertainment Company. With its mission to entertain the world, Gearbox brings highly creative AAA development studios, North American publishing capabilities, and a robust IP portfolio, including critically acclaimed and commercially successful franchises like Borderlands, Brothers in Arms and Homeworld. Since the transaction was closed in April 2021, Gearbox has formed Embracer's seventh operative group and operates as an independent studio focusing on premium interactive gaming experiences”.

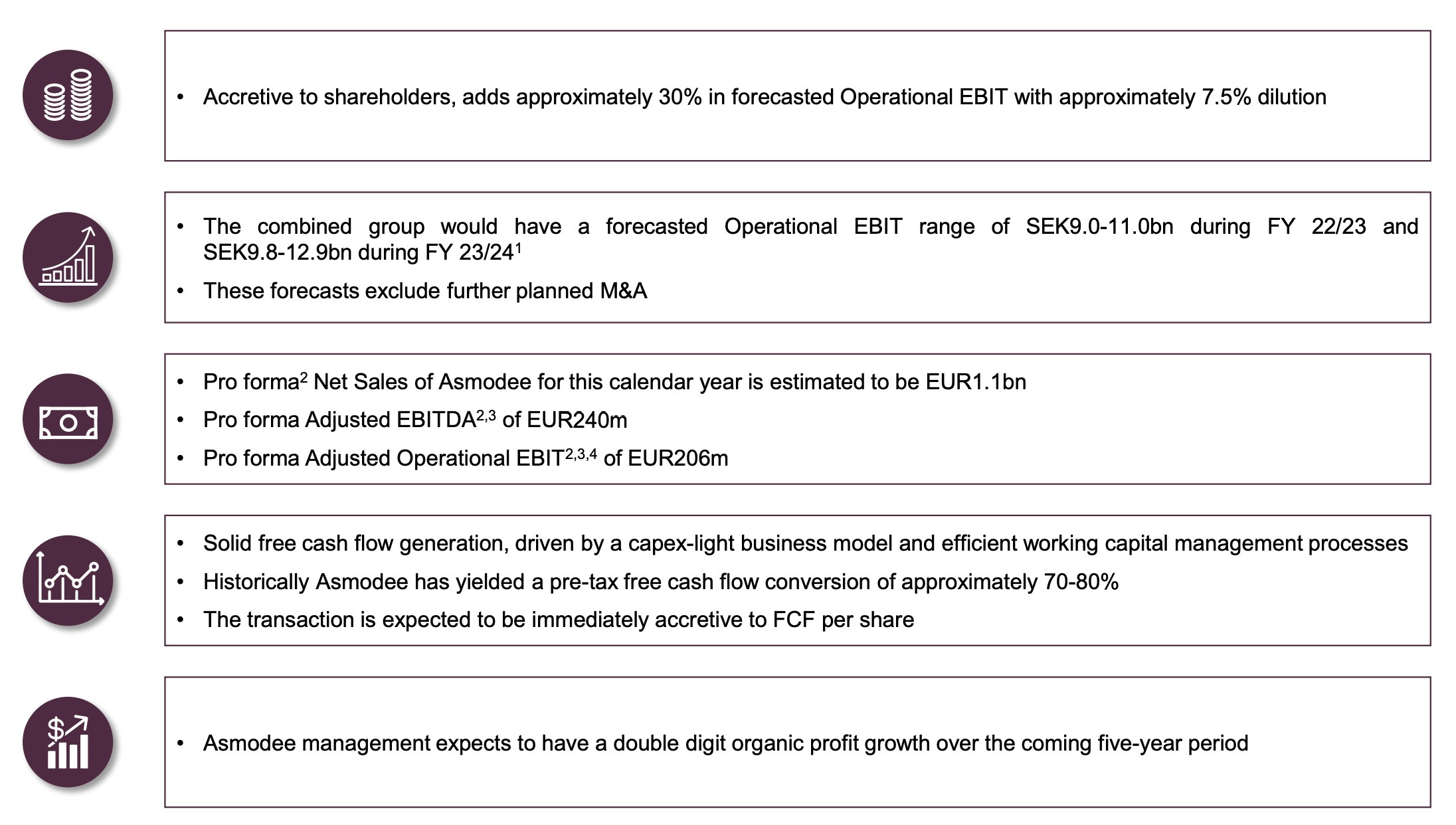

1.9. Asmodee (France): in the Q3 2021/2022 report, the creation of the ninth operating group after the conclusion of this acquisition was announced, which will continue to operate independently. It is a leading international creator and distributor of board games, trading cards and digital board games. Asmodee's proforma net sales for this calendar year are estimated at EUR1.1bn, proforma adjusted EBITDA at EUR240m and proforma adjusted operating EBIT at EUR206m.

1.10. Dark Horse (USA): in the Q3 2021/2022 report, the creation of the tenth operating group was announced after the conclusion of this acquisition. With this purchase, Embracer now controls more than 300 pieces of intellectual property and strengthens its capabilities by adding expertise in content development, comic book publishing, and TV and film production. It is one of the largest comic companies in the USA, behind Marvel and DC Comics.

2. Business Area: Partner Publishing/Film

2.1. Koch Films (Germany): “Embedded in the Koch Media group, Koch Films is a leading independent film publisher and distributor in German-speaking Europe and Italy operating in all film sales channels. The catalog consists of thousands of films/TV series in all genres, it is particularly strong in anime, cult classics and world cinema movies”.

2.2. Game Outlet Europe (Sweden): “Game Outlet Europe AB is an independent niche distributor of reprinted physical video games, gaming hardware and retro gaming hardware located in Karlstad, Sweden. The company was founded in 1994 by the Embracer Group's CEO Lars Wingefors”.

2.3. Quantic Lab (Romania): “Quantic Lab, based in Cluj-Napoca, Romania, is a software outsourcing company specialized in Quality Assurance (“QA”), localization and User Experience for gaming and applications. Quantic Lab was founded in 2006 by Stefan Seicarescu, current CEO, and has since grown, from being a start-up with a small team of 12 persons, into a leading QA company with more than 60 active clients and more than 350 employees in three office locations in Romania and one office in UK”.

2.4. Grimfrost (Sweden): “Grimfrost is a global leader in high-quality Viking merchandise, located in Karlstad, Sweden and comprises a team of 12 employees. While the primary business model is business-to-consumers (B2C), Grimfrost also supplies costumes and assets to TV and movie productions (e.g. Game of Thrones and Vikings) and reproductions for museums”.

One aspect that caught my attention is the decentralized structure that Lars has built in his organization: the holding structure, Embracer, is a link between the different elements the group has. The CEO of one of the subsidiaries, in the webcast Q3 2021/2022 (around 01:15:00), mentions that it is a common practice that the different subsidiaries communicate and ask each other for help, even if this is not done using any formal channel. Apart from the above, belonging to Embracer allows them, for example, to obtain financing by obtaining credit or raising capital under more favorable conditions than those they would obtain if they were independent. In the same way, the holding company is in charge of giving support in the most routine tasks, such as the legal, logistical aspects, among others, granting the subsidiaries freedom to focus on the creative aspect and game development, which is what brings cash flow. Does the subsidiary not have a publisher arm? The publisher arm of the group is used. Does the subsidiary have a poor legal department? You can close it and you can use the one from EMBRAC.

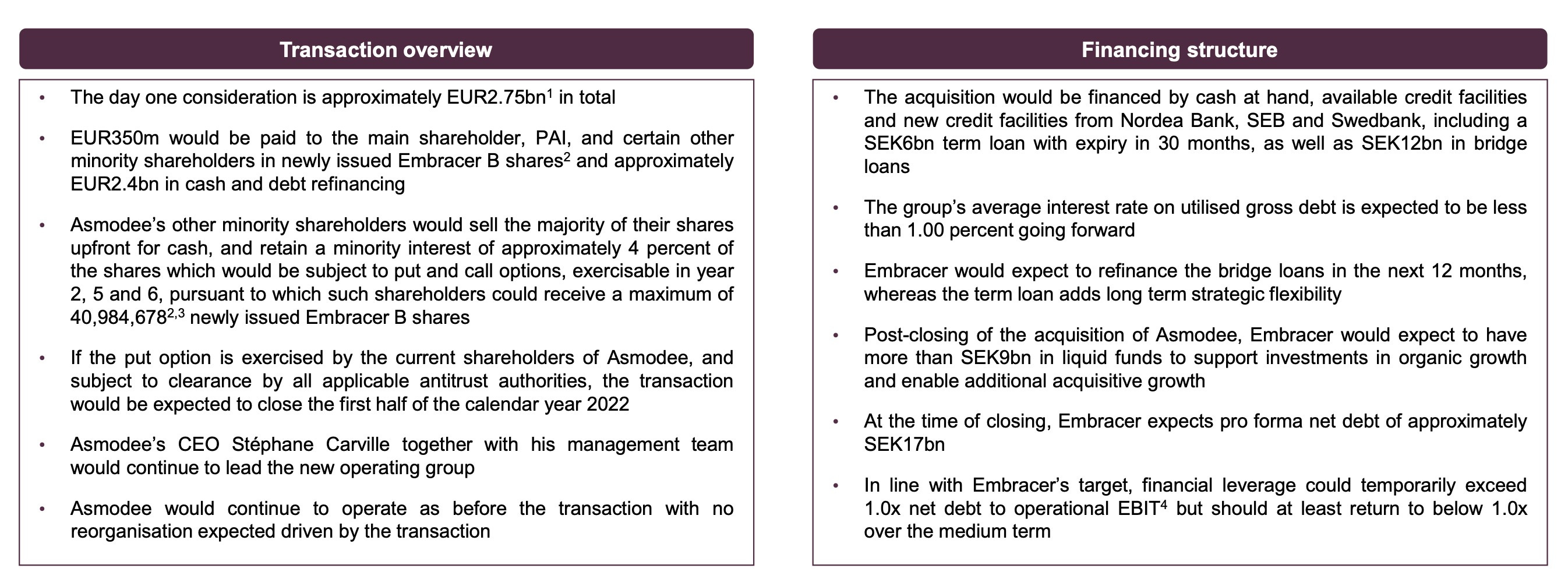

I would like to draw your attention to Asmodee, one of their biggest and most recent acquisitions, for which they paid around EUR 3B. Part of the payment is conditioned on reaching certain goals, both financial and performance. This French company founded in 1995 is an international publisher and distributor of table and card games, and sales in 2021 are around EUR 1B, which is equivalent to adding approximately SEK 10B to EMBRAC's sales. Let's see the reasons that led our company to acquire Asmodee:

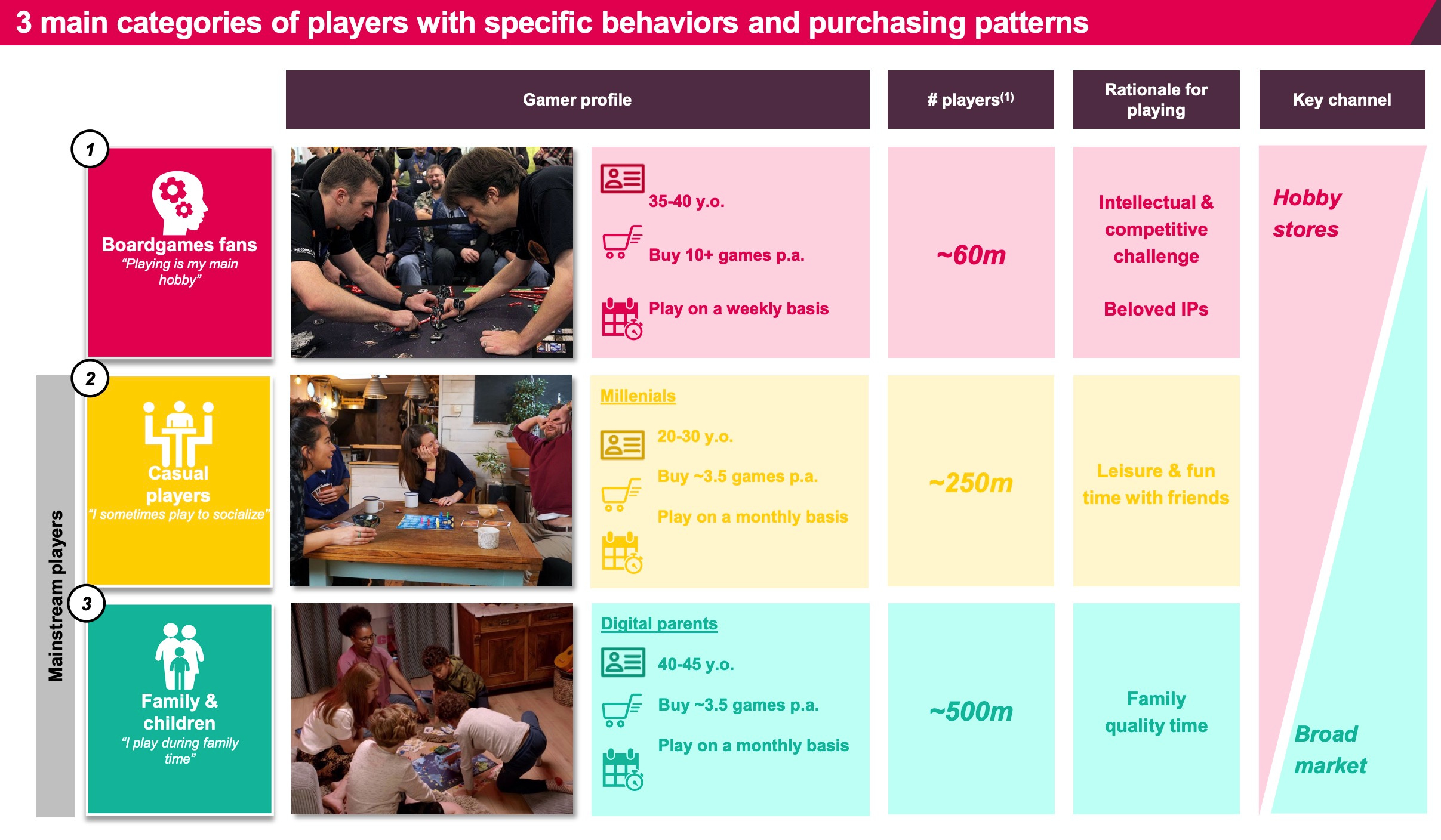

Asmodee's CEO, Stéphane Carville, mentions that in their local market, France, they barely have a 25% market share, and 7% of the US market, so they still have ample room to grow. In addition, the market in which they operate is highly fragmented, which has allowed them to make more than 50 acquisitions. One of the factors of its success is its low Capex (the production of board and card games made of plastic, paper and cardboard is not too demanding, and part of the process is outsourced), which explains its high profitability. On the other hand, Asmodee has identified its type of client and has classified it into 3 categories: Boardgames Fans, Casual Players, Family and Children.

Like Embracer, Asmodee has a decentralized structure with 22 game development studios and more than 300 pieces of intellectual property. In addition, they have subsidiaries that distribute this type of game in 50 countries and outsource this task in those jurisdictions where they do not have a direct presence. Their process of creating a game, from the conception to its concretization in a product, takes between 12 to 24 months. In Q3 2021/2022, the following is mentioned about the acquisition of Asmodee and Dark Horse: “Following the closing of these transactions, Embracer Group will have one of the most diversified portfolios of Intellectual Property in the gaming industry. Reliance on any individual title or intellectual property is expected to be less than five percent of group net sales, which will make our operating performance even more predictable”. We look at income diversification. For more details, you can check this link.

Now, a very important point to mention is that the M&A strategy has been developed, in part, using shares: as part of the payment, EMBRAC has used its own shares as currency for the management of the acquired company, which aligns them with the other shareholders and prevents them from falling into the employee mentality.

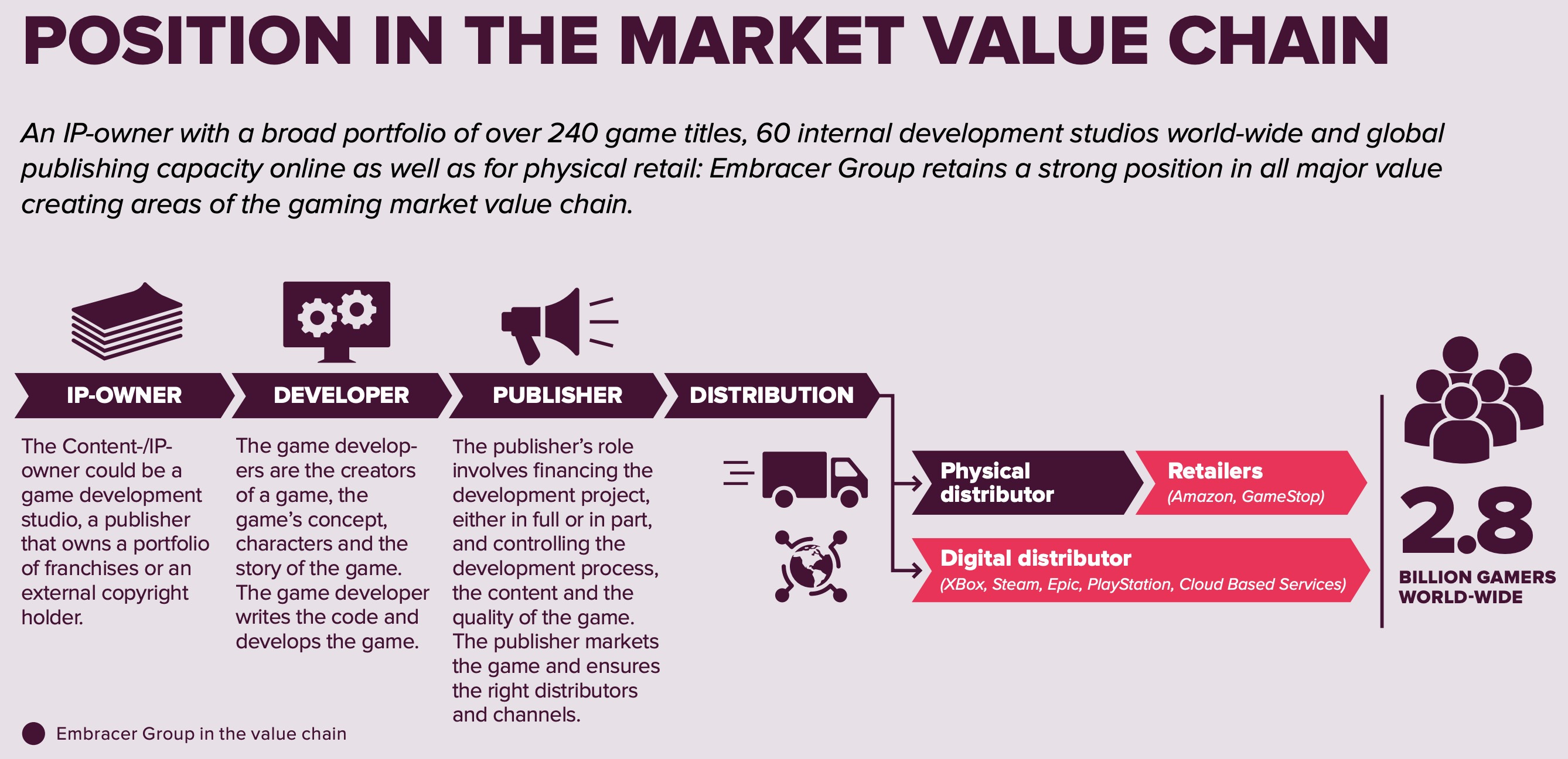

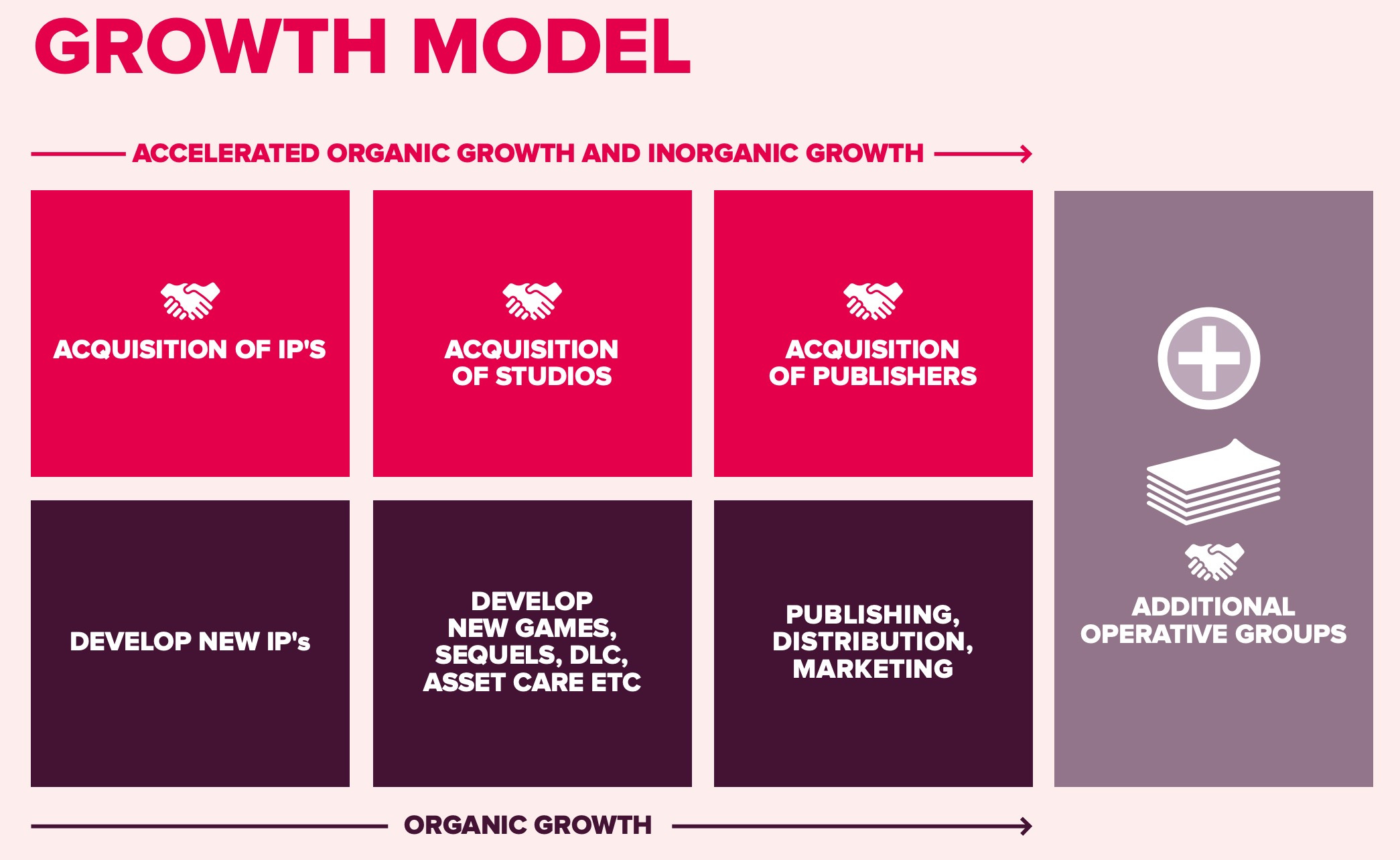

Finally, Embracer itself recognizes its place within the market value chain: Intellectual Property, Developers, Publishers and Physical Distribution. Similarly, we are presented with a graph of the growth model they have chosen to develop.

Regarding acquisitions, their model is based on allowing absolute creativity for the acquired companies: they try to ensure that the acquisition only brings benefits in the form of internal connections and financing, they do not try to take absolute control of each decision. In addition, the companies that join the family must have a management that thinks in the long term, just as the management of the parent company does.

4. Financial Overview

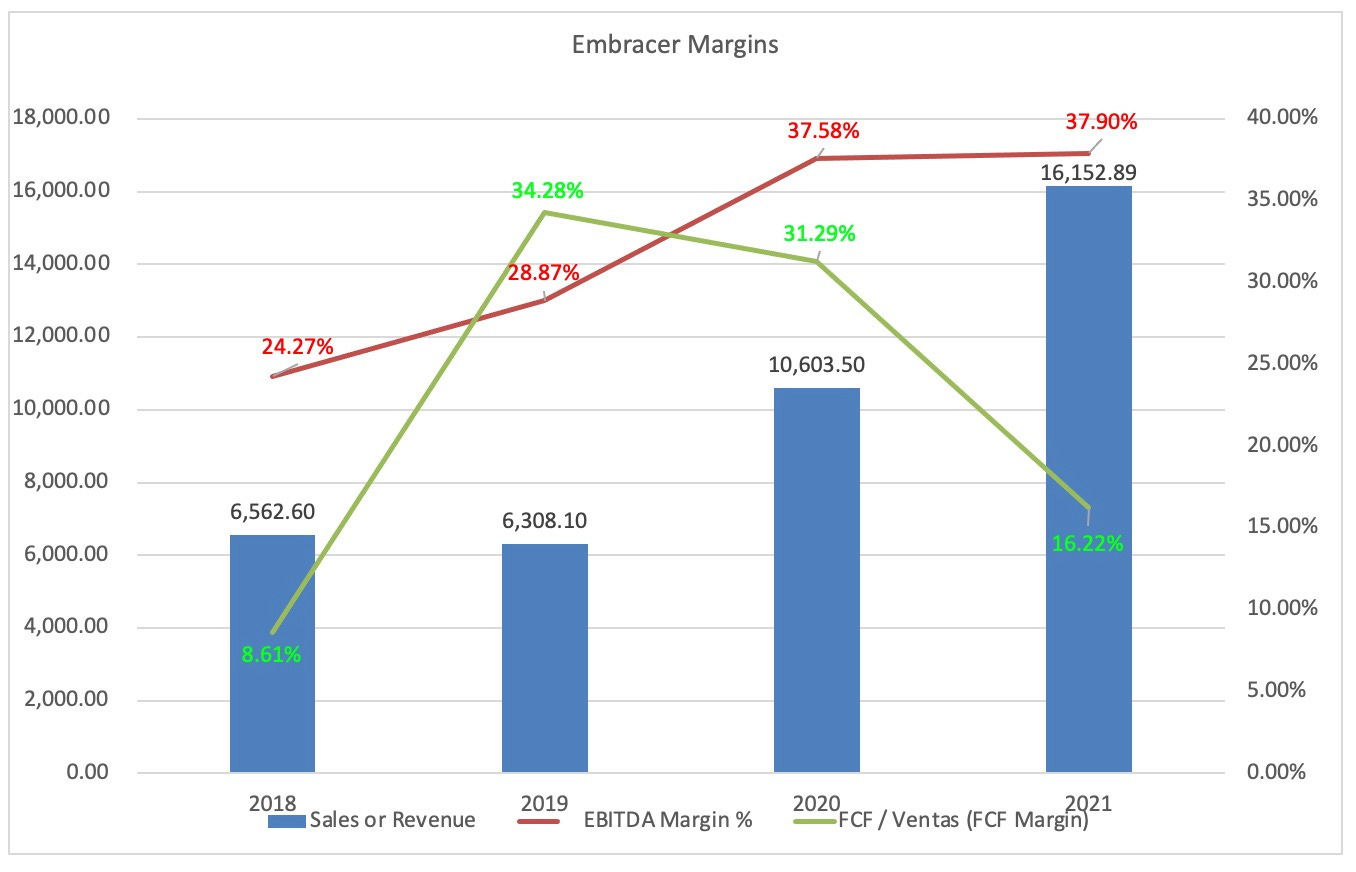

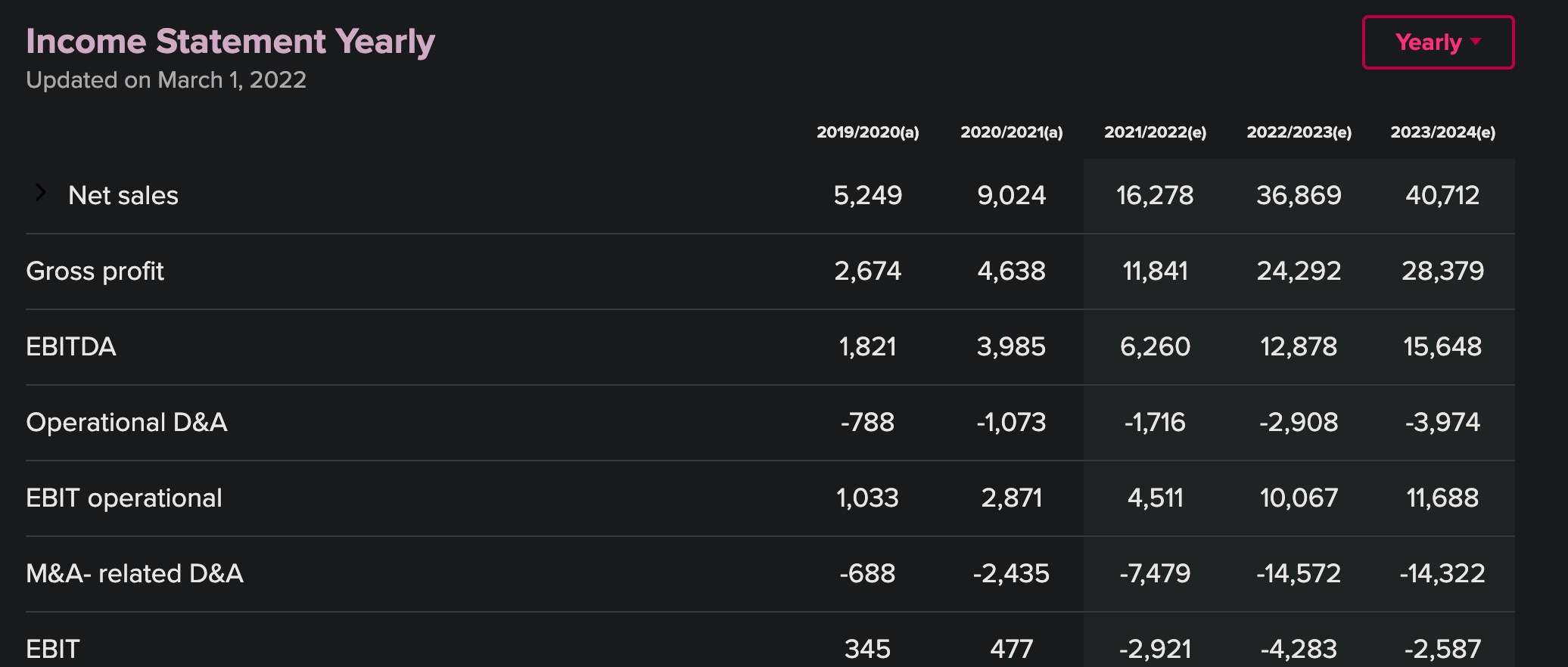

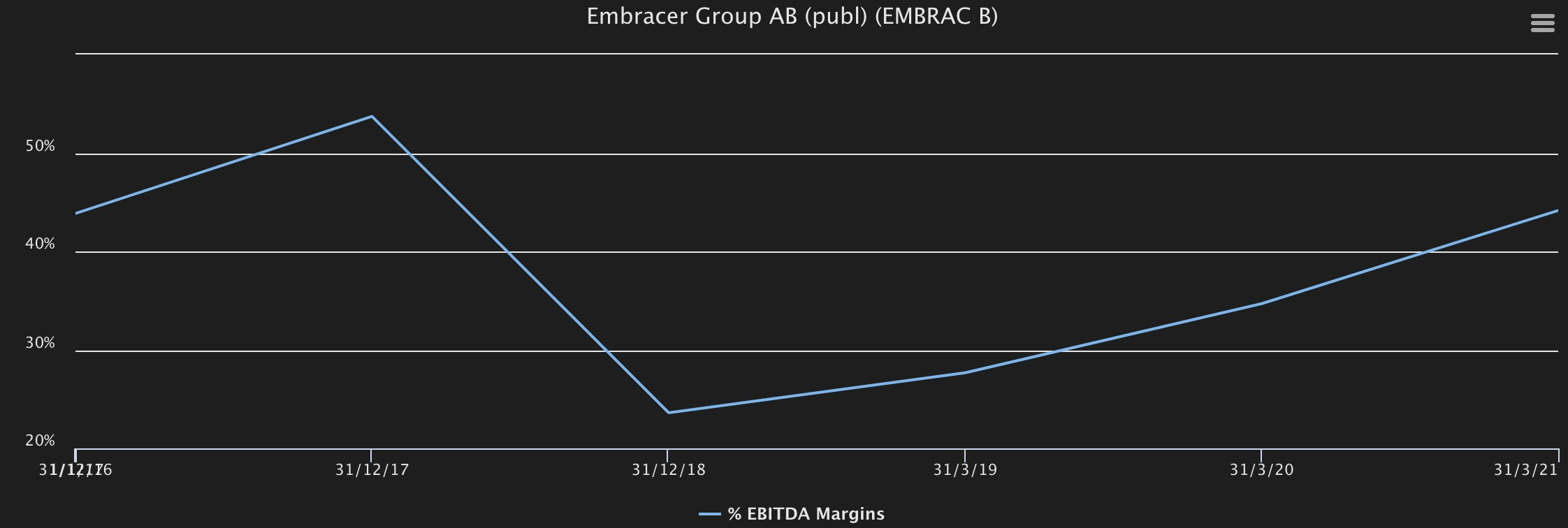

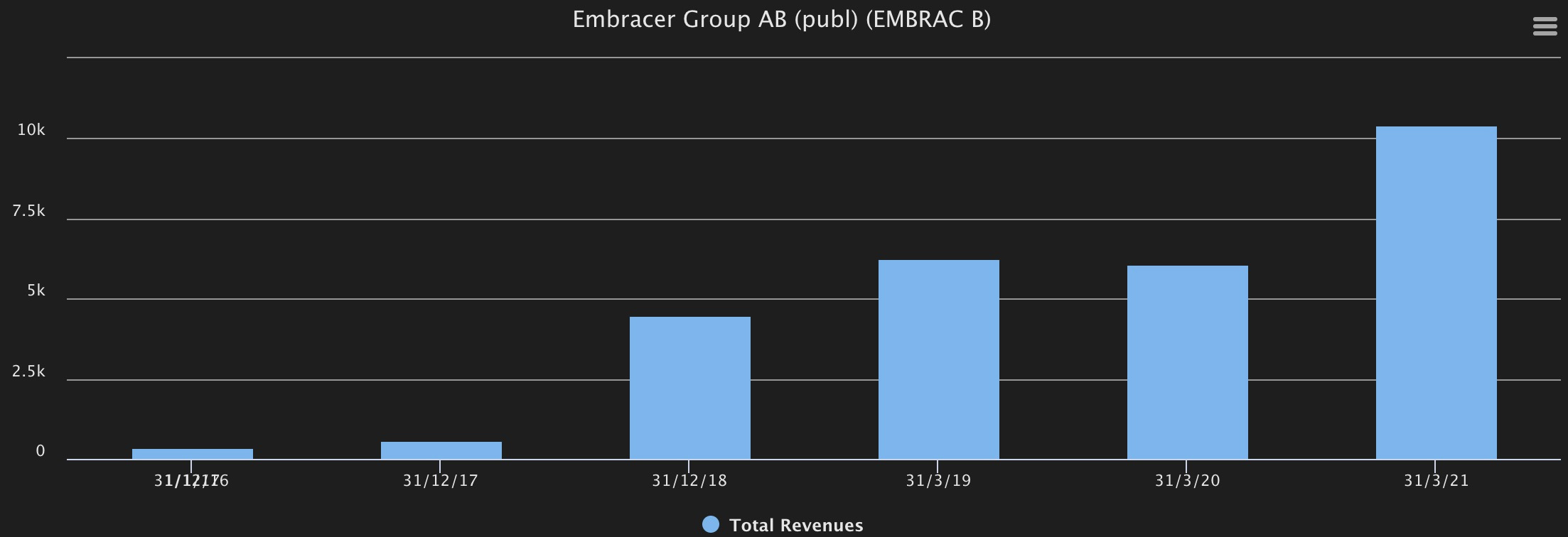

Having seen the above, let's review the financial side of Embracer. It should be mentioned that analyzing this aspect is one of the most challenging, given the structure and continuous development of the company through acquisitions, which have not stopped. EMBRAC's Operating Units are evolving and changing, as seen in the latest annual and quarterly reports: FY 2018/2019, FY 2019/2020, FY 2020/2021 and Q3 2021/2022. Below are the margins of the consolidated results that the group has presented over the years (bear in mind that the FCF Margin that appears in 2018 is distorted for not having considered the working capital of 2017; in addition, the information of 2021 is still a projection because the annual report FY 2021/2022 has not been published yet).

Sales have been growing at a CAGR of approximately 25% from 2018 to 2021, and EMBRAC has posted a growing EBITDA Margin from 25% to approximately 37% today. The FCF remains unstable due to ongoing acquisitions and additions to the consolidated financial statements. Below, we present the financial projections that our company shows on its website (it should be noted that the projections were updated on March 1, 2022, after the conflict in Ukraine began).

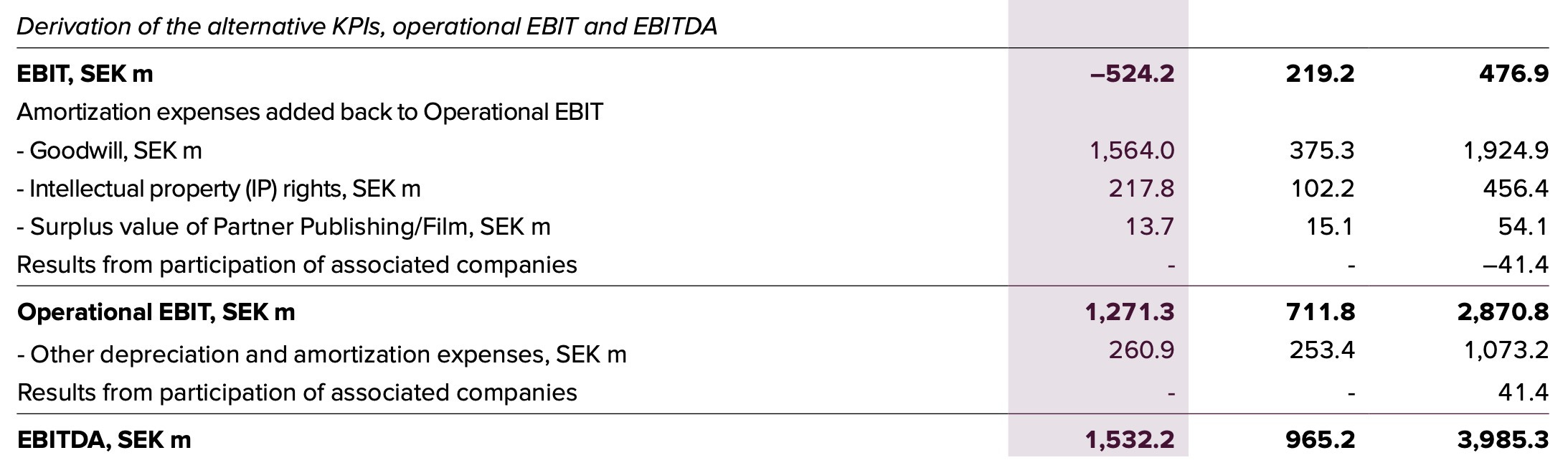

For those wondering what Operational EBIT is, it is a non-GAAP metric presented by the company itself and lower than the EBITDA calculated by EMBRAC. Below is a table showing how our company builds it.

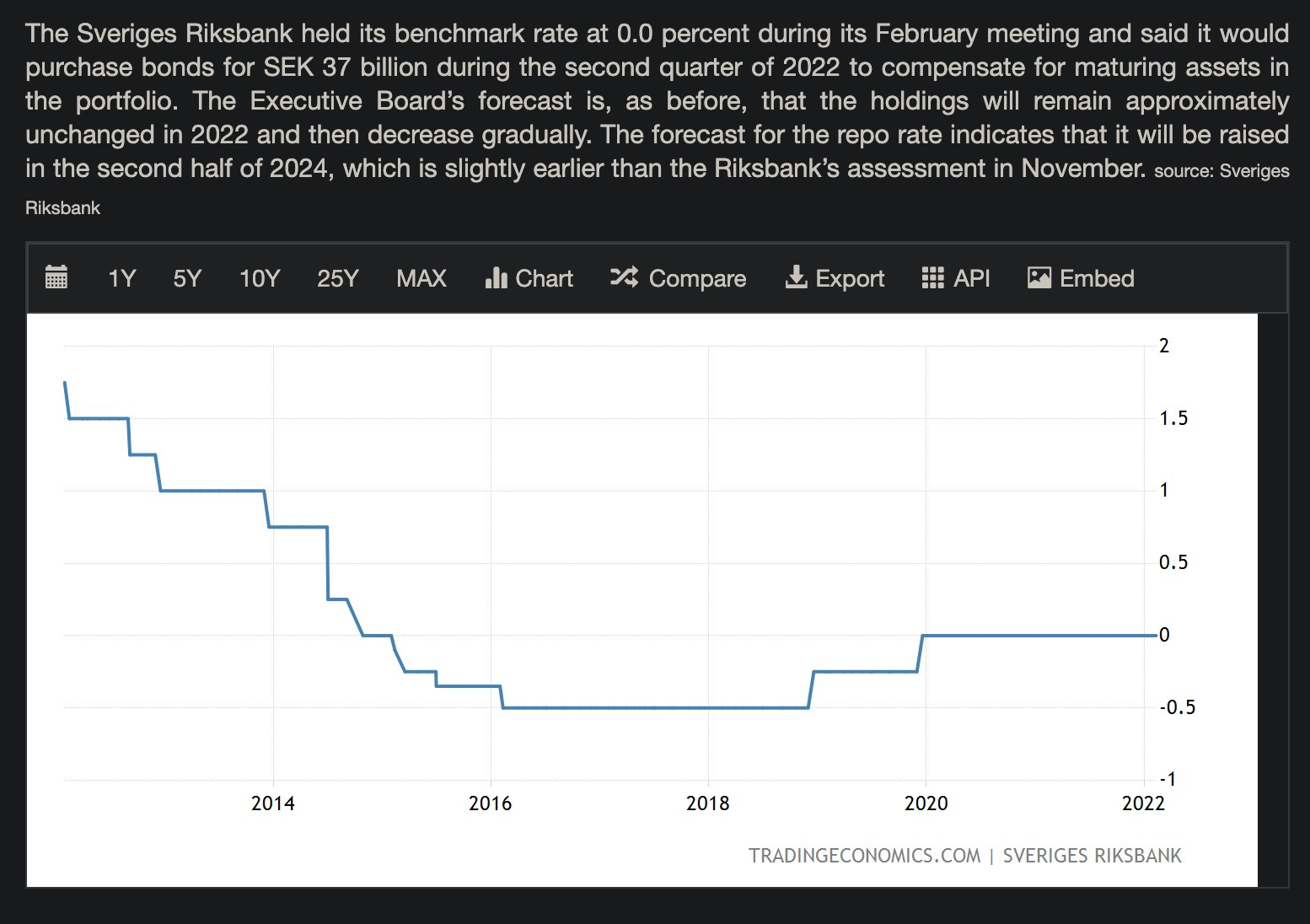

The Working Capital/Sales has been reduced over time, and the ROIC is distorted due to the acquisitions. Due to the acquisition of Asmodee, EMBRAC has taken on debt that is likely to make the company go from Net Cash to Net Debt in the short term, although I estimate it will return to Net Cash due to its history of generating FCF and its Cash reserves. The debt was acquired in a favorable environment of interest rates in SEK, as shown in the following graph:

Embracer's goal is to complete 90 development projects for the 2021/2022 period, which we will find out when the annual report for that period is published.

In the Q3 2021/2022 report, the following is mentioned: “The objective of our capital allocation is to drive profitable growth, and the model seems to be working. We believe that the highest potential for value creation is by maximizing long-term profitable organic growth. We have a record 216 ongoing development projects. More than 95% of our capitalized development spend is allocated to the development of upcoming premium games. Our pipeline now has more than 25 AAA development projects planned for release until March 2026 with the potential to drive significant organic growth”.

Regarding the financial future of EMBRAC, in Q3 2021/2022 we observe the following: “Several of the businesses acquired over the past year have a low capital intensity. With strong organic growth ahead, we anticipate gradually growing free cash flow. Our diversification is increasing and revenues become more predictable. Our belief is that a strong balance sheet is a tool for long-term value creation, as we always act from a position of strength”.

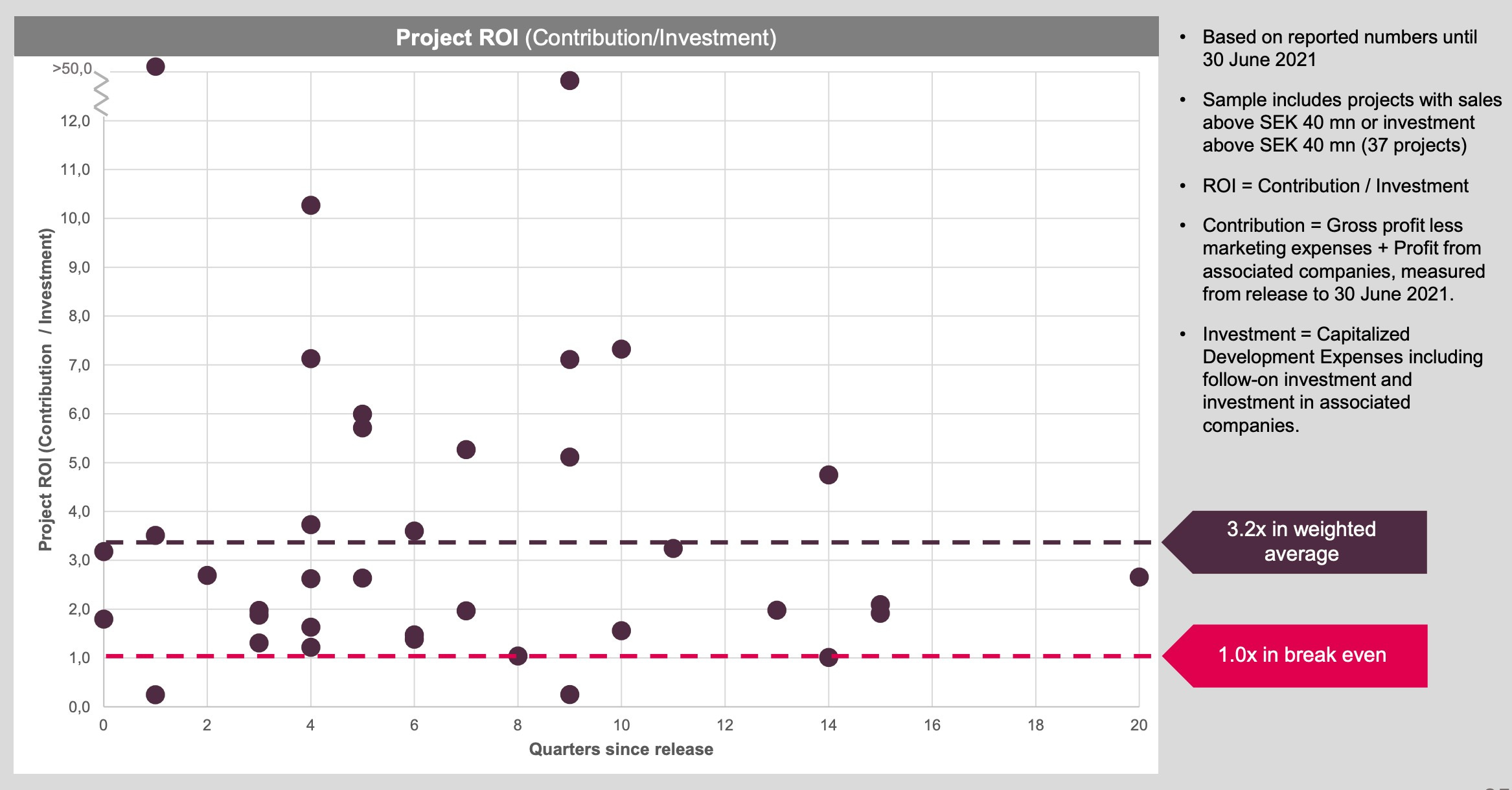

According to the transcript for Q3 2021/2022, 70% of revenue is classified as recurring, in contrast to Q3 2020/2021, which was 35%. As for organic growth this quarter, the CFO mentioned a growth of 19% (SEK 600M) from 3.1B SEK to 3.7B SEK. To finish this section, let's look at the following table with information regarding the profitability of the projects developed by our company (the sample is 37 projects, the X axis represents the number of quarters that have elapsed since the launch of a game and the Y axis represents how many times the revenue contribution has exceeded development spending):

In addition, as they mention in their FY 2020/2021 annual report, they allocate most of their FCF to reinvestment to generate organic and inorganic growth.

5. Moat

Intangible Assets: It is clear that in a game and video game creation business, both brands and intellectual property become relevant. Given this, the acquisitions of Asmodee and Dark Horse make sense: it is not only about acquiring studios capable of creating video games, but also intellectual property that allows content to be generated.

Scale: Given Embracer's geographical scale and diversification, it is easier for it to obtain favorable credit and financing conditions than smaller companies, this in different currencies (EUR, SEK, USD, etc.), in addition to offering ready-made departments that acquirees can use (legal, marketing, etc.).

6. Management

Management is of great importance in our company (see here). As already mentioned, the CEO is Lars Wingefors, who also founded the group.

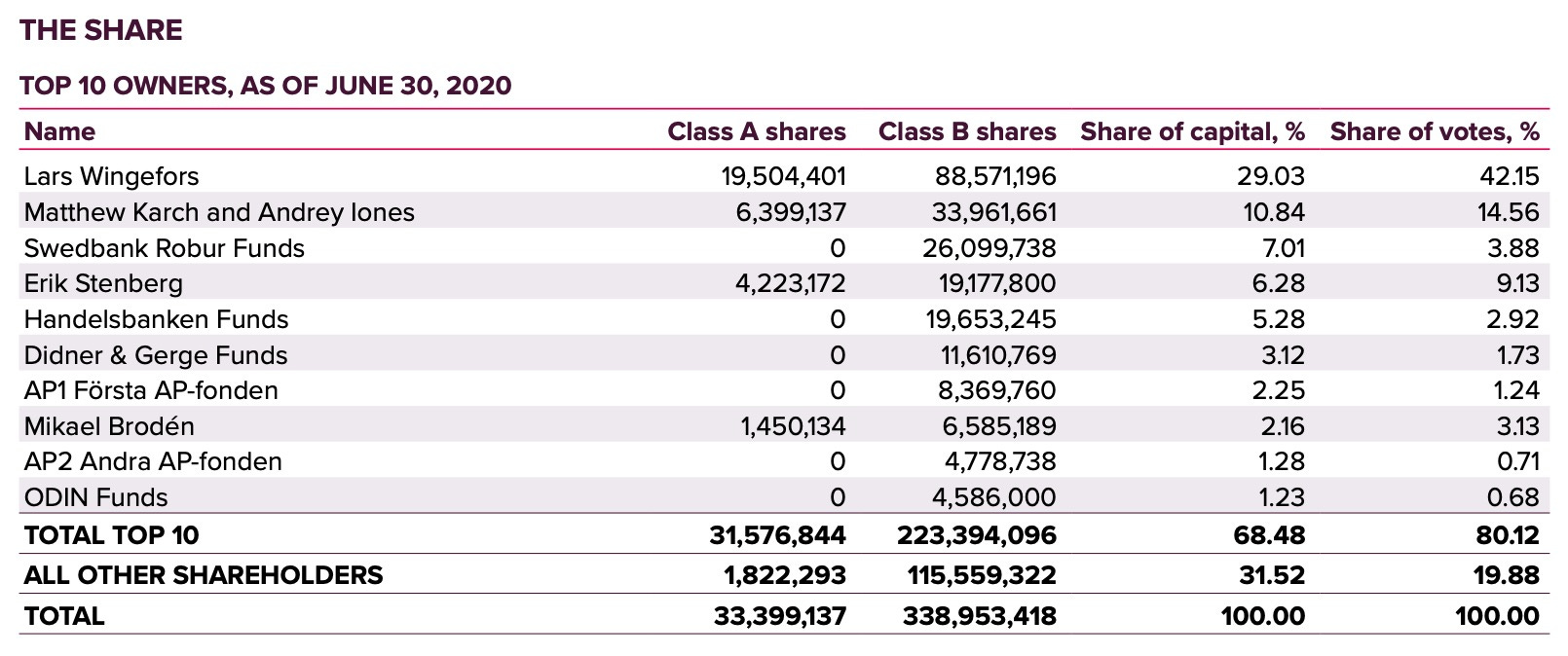

As Warren Buffett likes it, management has skin in the game, as can be seen in the table below (see here):

Let's put the previous table of December 2021 with the 10 largest shareholders in relation to its version of June 2020:

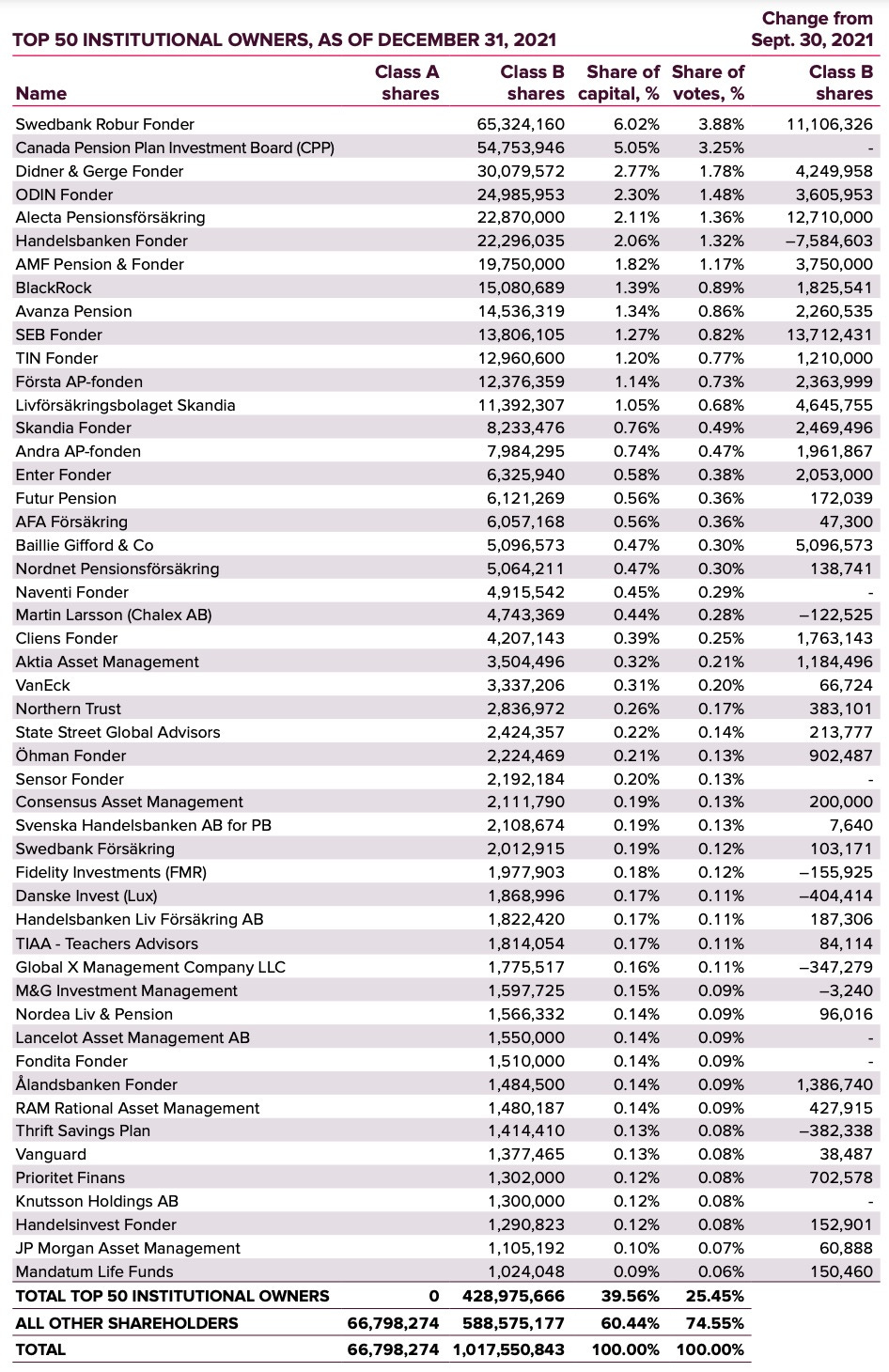

We note that, as of December 2021, the largest shareholder is Lars Wingefors through Lars Wingefors AB, which controls 24.21% of EMBRAC's capital and 43.48% of the votes. We also observe the existence of 2 classes of shares: class A has 10 votes per share, while class B has 1 vote per share. The class B was created in 2018 (see here) with the aim of expanding the shareholder base, preventing management from losing control by excessively issuing class A. Apparently, the objective was achieved, as can be seen in the following table of institutional shareholders as of December 2021:

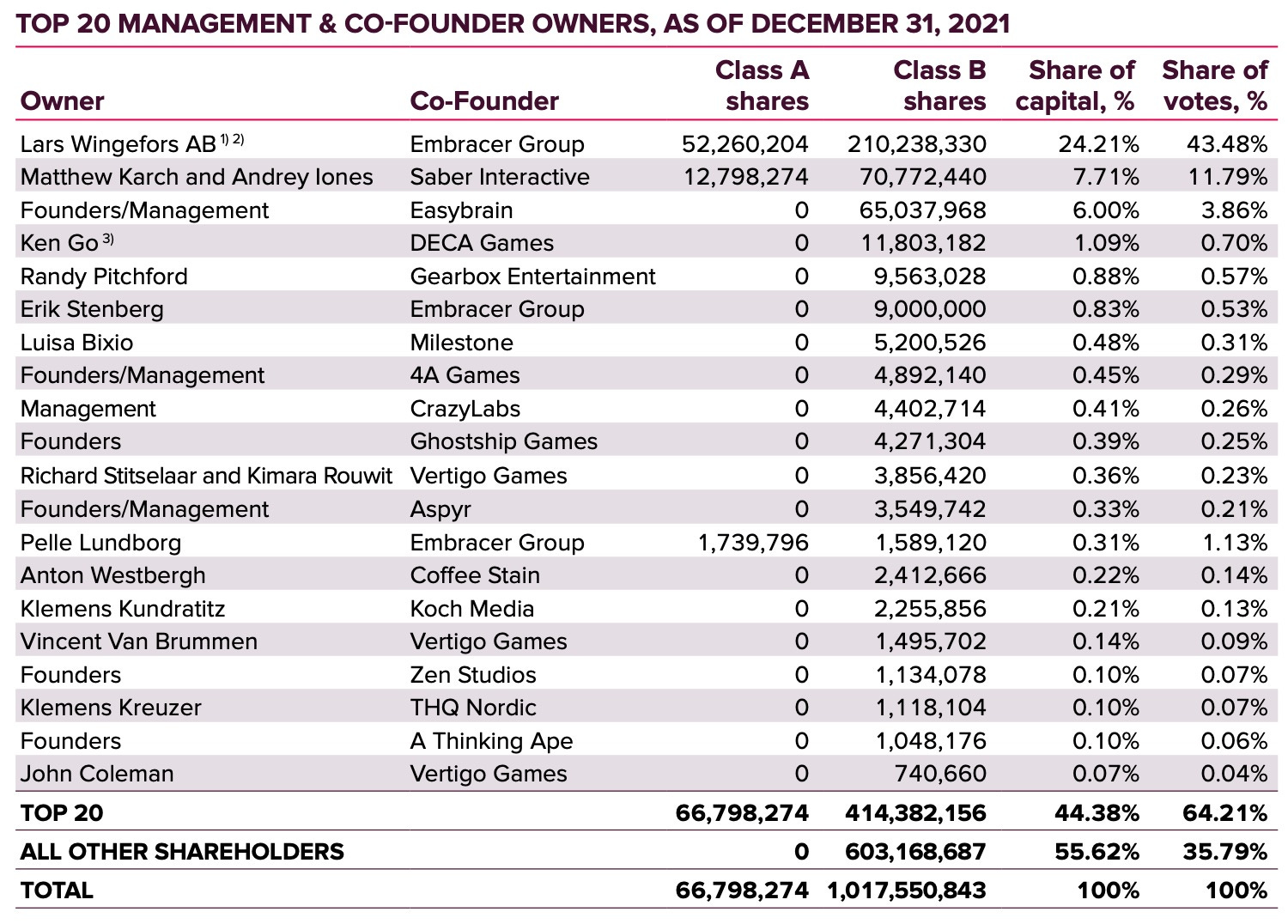

Do you want to see an even more beautiful table? For many of the acquisitions, apart from cash, EMBRAC has used shares as the currency to pay: the aim of this is to get the founders to maintain an entrepreneurial mindset and avoid a salaried one. Next, we look at share ownership among founders (entrepreneurs who decided to join Embracer are called like that):

John Coleman, the smallest co-founder in the table, has 740.66K shares, at an average price of SEK 80, this represents more than SEK 59M (over USD 6M). But let's go further: in the FY 2020/2021 report, it is mentioned that Embracer made a private placement of class B shares at an average price of SEK 162 in October 2020. What is special about this? The founders of the acquired subsidiaries consolidated their ownership of more shares through their participation in Lars Wingefors AB instead of owning them directly through their personal holding companies: this means that a percentage of the shares owned by the holding company Lars Wingefors AB belongs to them. This percentage has not been disclosed.

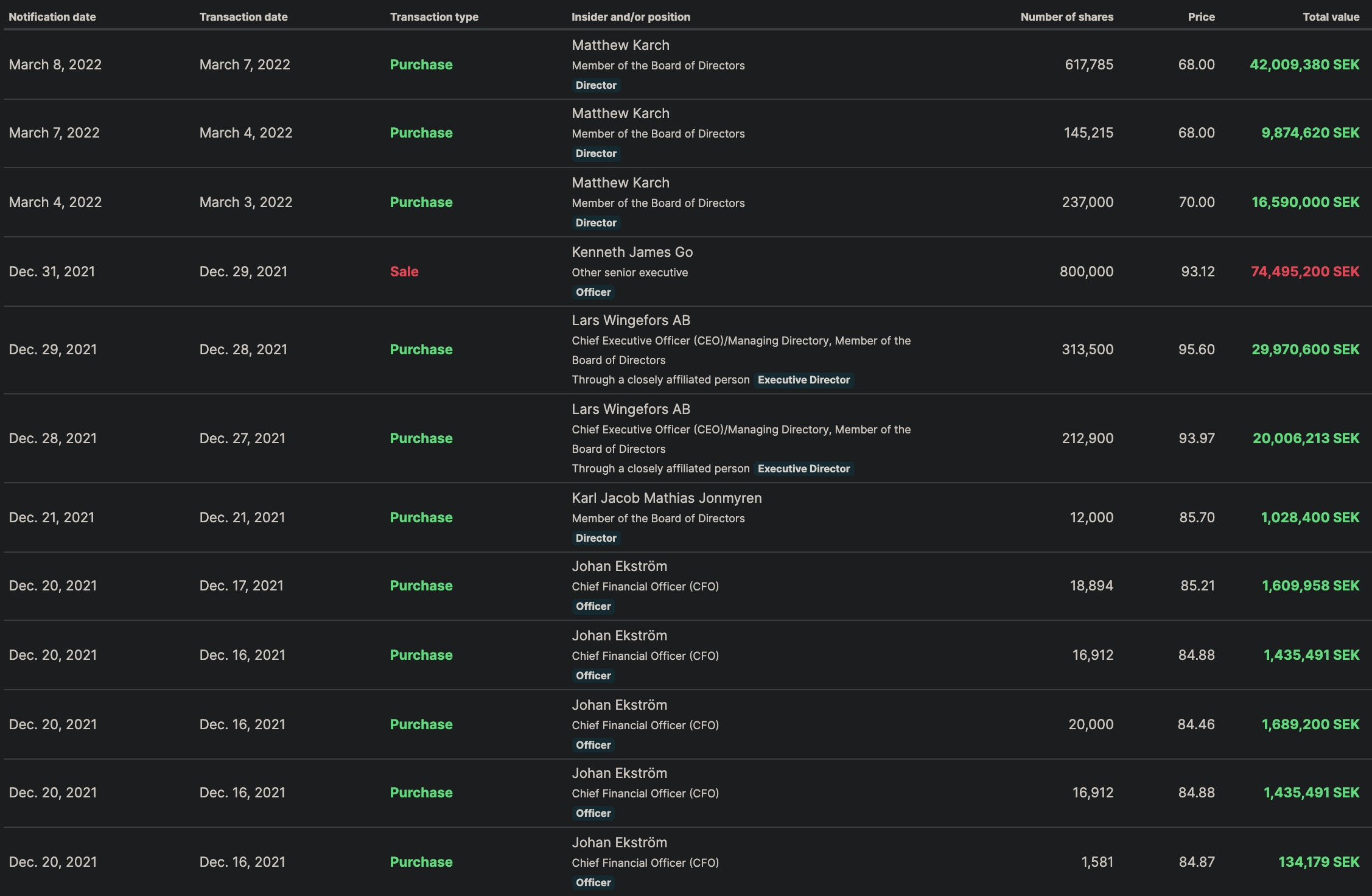

Given the above, we see that the issuance of shares is a key aspect of their acquisition strategy. Now, the CEO could establish a program through which he receives more shares to avoid being diluted and losing voting power each time EMBRAC increases capital. It would be the most comfortable and least risky for him, since he would not have to risk his own capital. However, to avoid the natural dilution of his acquisition strategy, Lars buys on the open market to preserve his decision-making capacity, and we also have Matthew Karch buying on the open market more than SEK 68M (USD 7M) in shares (see here):

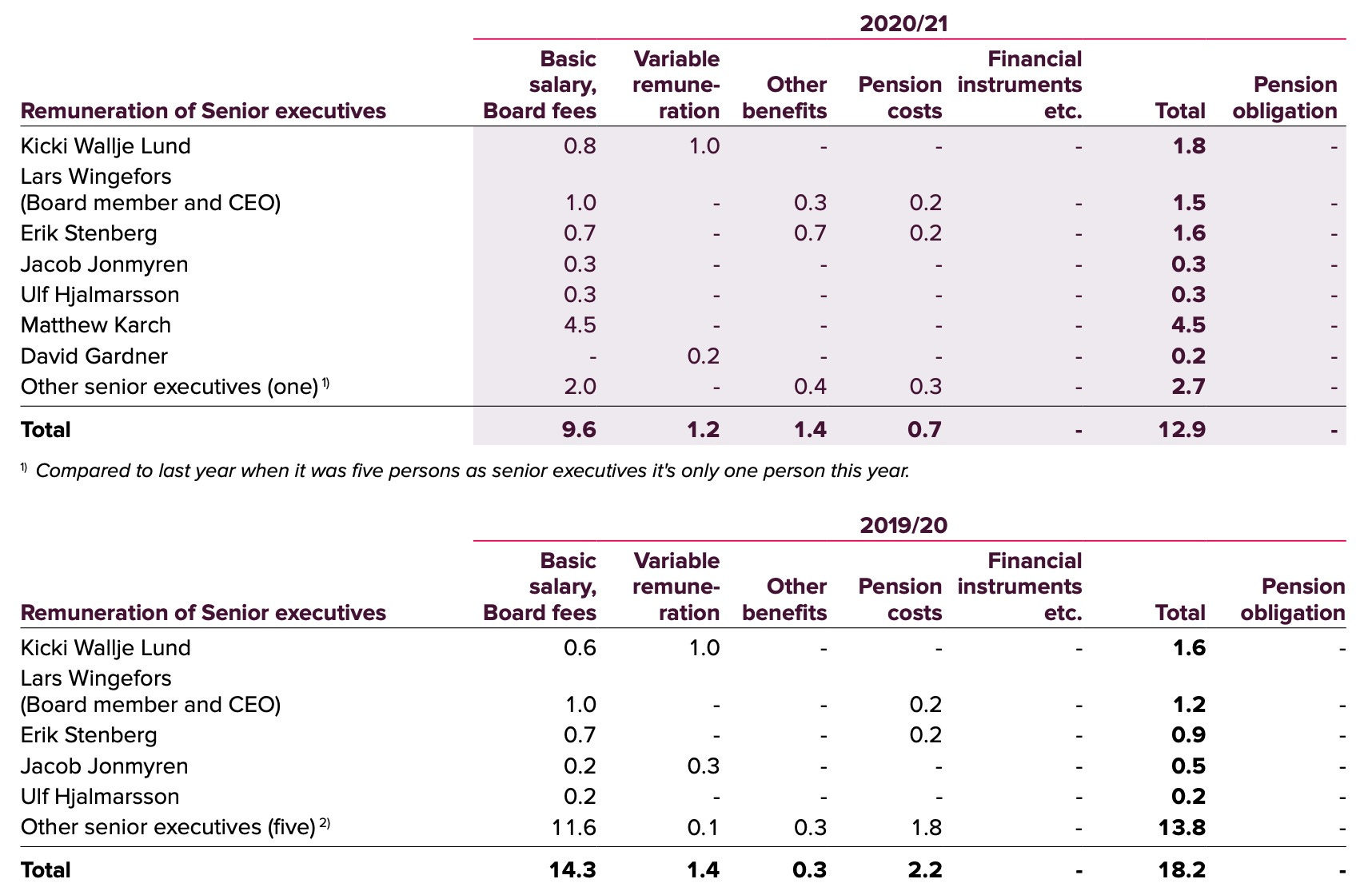

Regarding the compensation of the Board of Directors, we note that it is a very humble one for a company that capitalizes SEK 85B and has annual sales greater than SEK 10B (a CEO barely earning SEK 1M per year and a director earning SEK 4.5M):

Something that I personally liked a lot was reading the following in the FY 2020/2021 annual report: “Embracer Groups financial goal is to achieve long-term growth in shareholder value”. This is, without a doubt, possible since we have a management with a lot of skin in the game.

Finally, to conclude this section, I want to highlight the honesty shown by the CEO in the Q3 2021/2022 Earnings Call about the performance of one of Embracer's projects: "Chorus, the title developed at Deep Silver Fishlabs in Hamburg has been well received by the communities and on Steam with players. However, commercially, that title has not reached the expectations from the management”.

7. Industry

According to Fortune Business Insights (see here), the TAM of video games is projected to grow at a CAGR of 13.2% in the period 2021-2028, reaching a size of USD 545B in 2028. In the FY 2020/2021 report, Embracer itself presents projections and comments on the evolution they see in their industry in the coming years. Therefore, below I share the information that they showed in their regulatory document.

About the industry, we have the most recent information in the Q3 2021/2022 report, in which the following table is presented and these estimates are given:

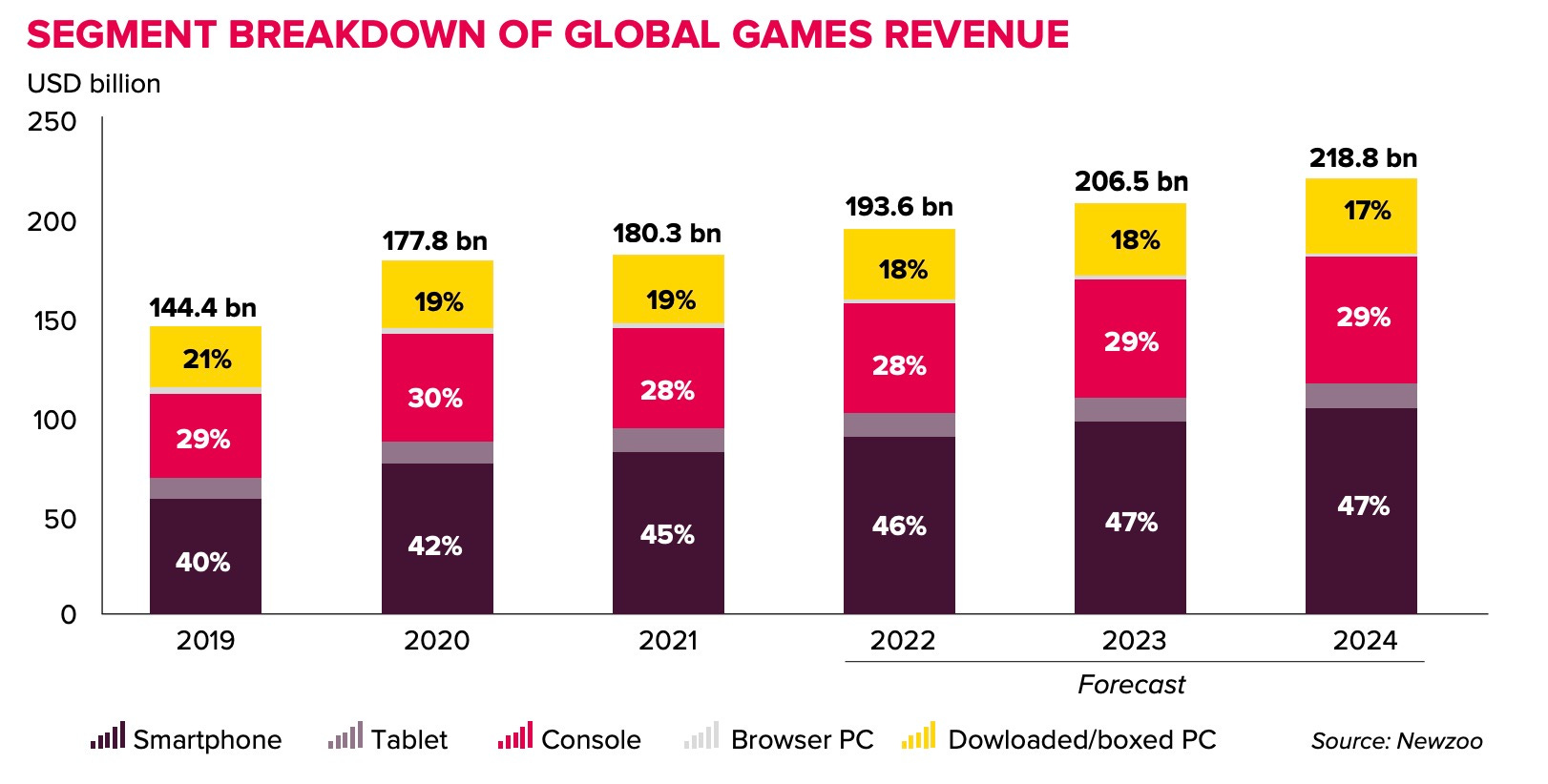

1. Video games market in 2021: “The 2021 games market is assessed to have generated an increase in consumer spending of +1.4%, in spite of previous expectations of a slight post-pandemic slowdown. Global market, including console, mobile, PC and free-to-play but not hardware, had an estimated gross turnover of USD 180 billion in 2021*. There are more players than ever before, now 3 billion in total globally, a growth of +5%*. And interest in gaming has also never been higher with Twitter reporting gaming posts up +14% in 2021. Looking further ahead for the global games market, Newzoo predicts that it will continue to grow at a CAGR (2019 to 2024) of +9% to reach USD 219 billion in 2024, passing the coveted USD 200 billion threshold in 2023”.

2. Mobile Gaming: “Mobile gaming is driving much of the market growth. The segment is estimated to have seen an increase of +7% in 2021 up to USD 93 billion* representing over half of the total games market. The pandemic has had significantly fewer negative impacts on mobile, which relies more heavily on in-app purchases, and whose development process has been less affected by home working. Growth figures are in spite of limitations in game approvals in its largest market, China as well as changes to Apple's IDFA for advertising. looking forward, a healthy market growth CAGR of +11% is expected between 2019 and 2024*. Embrace Group is now highly engaged in this sector, notably from its recent acquisitions CrazyLabs and Easybrain”.

3. The Console Market: “Whilst well up on 2019 revenues, the console segment is estimated to have fallen short of the pandemic-fueled highs of 2020, slightly declining in 2021 by -7%*. Widespread home-working of development teams has caused some delays to several highly anticipated games. While next-generation consoles are selling in higher numbers to their previous versions, the semiconductor crisis has led to a large shortage of PlayStation 5 and Xbox Series consoles. As a result, the console software market is still dominated by the older version formats, such as PS4 and Xbox One (which are declining year-on-year) and Switch (which is still performing well). The transition to a software market largely dominated by the next-gen formats, once console supply catches up, is expected by Sony to happen in the last quarter of 2022. This point, combined with the high number of big games coming (existing ones as well as those delayed) points to a strong year for the console segment in 2022”.

4. The PC Market: “The PC Market had another great year, maintaining a stable revenue performance, declining only marginally (-1%) versus the record 2020 year. Steam continues to break its own previous records with the number of its concurrent users, reaching its highest yet, some 30 million gamers in January 2022”.

5. VR: “The holiday period of 2021 was solid for the VR segment, with the Oculus Quest 2 now a successful and dominant hardware performer. And proof of its popularity and success is seen by the fact that the Oculus app (which you need to run the hardware) topped the iOS App Store and Google Play charts in the US during the last week of the year, reaching an estimated 13M global lifetime downloads (with 10% coming from the Christmas week alone) (SensorTower). And with Oculus's owner (Facebook) now rebranding to Meta, the company's new 'metaverse-first' strategy, is sure to further raise interest in VR. Beyond Oculus, some of the biggest brands in consumer tech have headsets on the horizon too, including Sony's PS VR2 and Meta's own Cambria. Embracer Group are well positioned to take advantage of this growing business through its VR studio Vertigo”.

6. Transmedia: “IPs expanding their universe across various media is nothing new, but there is a clear trend moving towards “games first” as the central IP. We have recently seen a high number of high-quality, commercially successful TV / film adaptations such as Netflix's The Witcher season 2 and Arcane (based around League of Legends). Still to come are Uncharted, Sonic 2, Super Mario movie and the Halo TV series (with Steven Spielberg as creative partner). From within Embracer Group, forthcoming films include Borderlands, an action/comedy with Eli Roth as director and a high-profile cast including Cate Blanchett, Kevin Hart, Jack Black, and Jamie Lee Curtis. This proves the value in brand building and the monetization possible across several media with having a stable of strong gaming IPs. Through the diverse portfolio of IP’s and following the acquisitions of Asmodee and Dark Horse, Embracer Group will be well positioned to benefit from transmedia IP´s”.

8. Peers

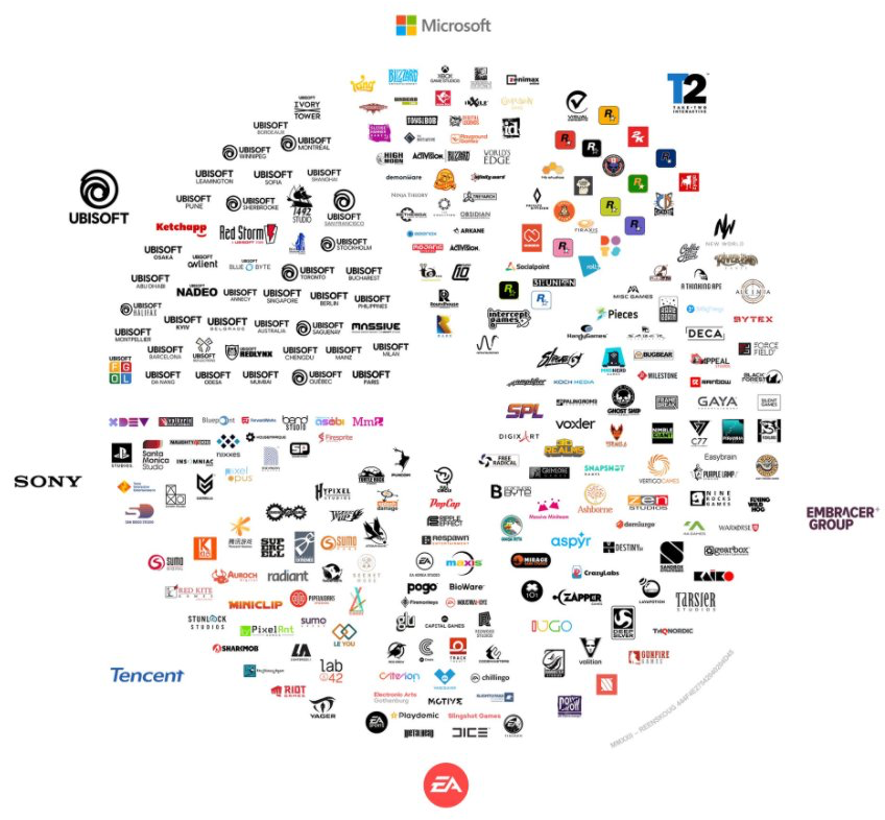

Embracer is part of an ecosystem of video game developers and publishers. Below we present a graph with the main players in this industry, although not all of these are directly comparable with our company (for example, Microsoft is highly diversified, so Sony and Tencent are).

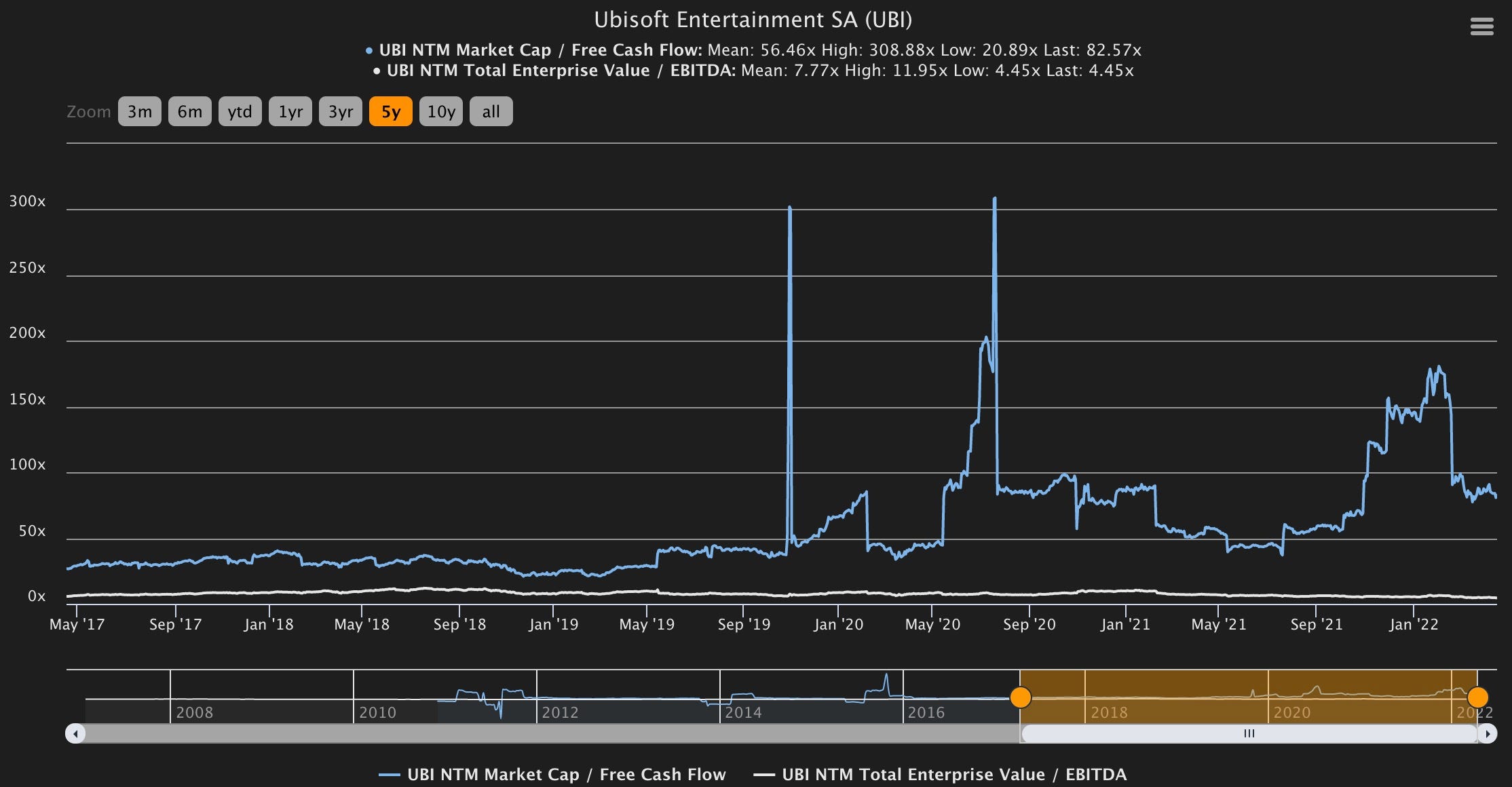

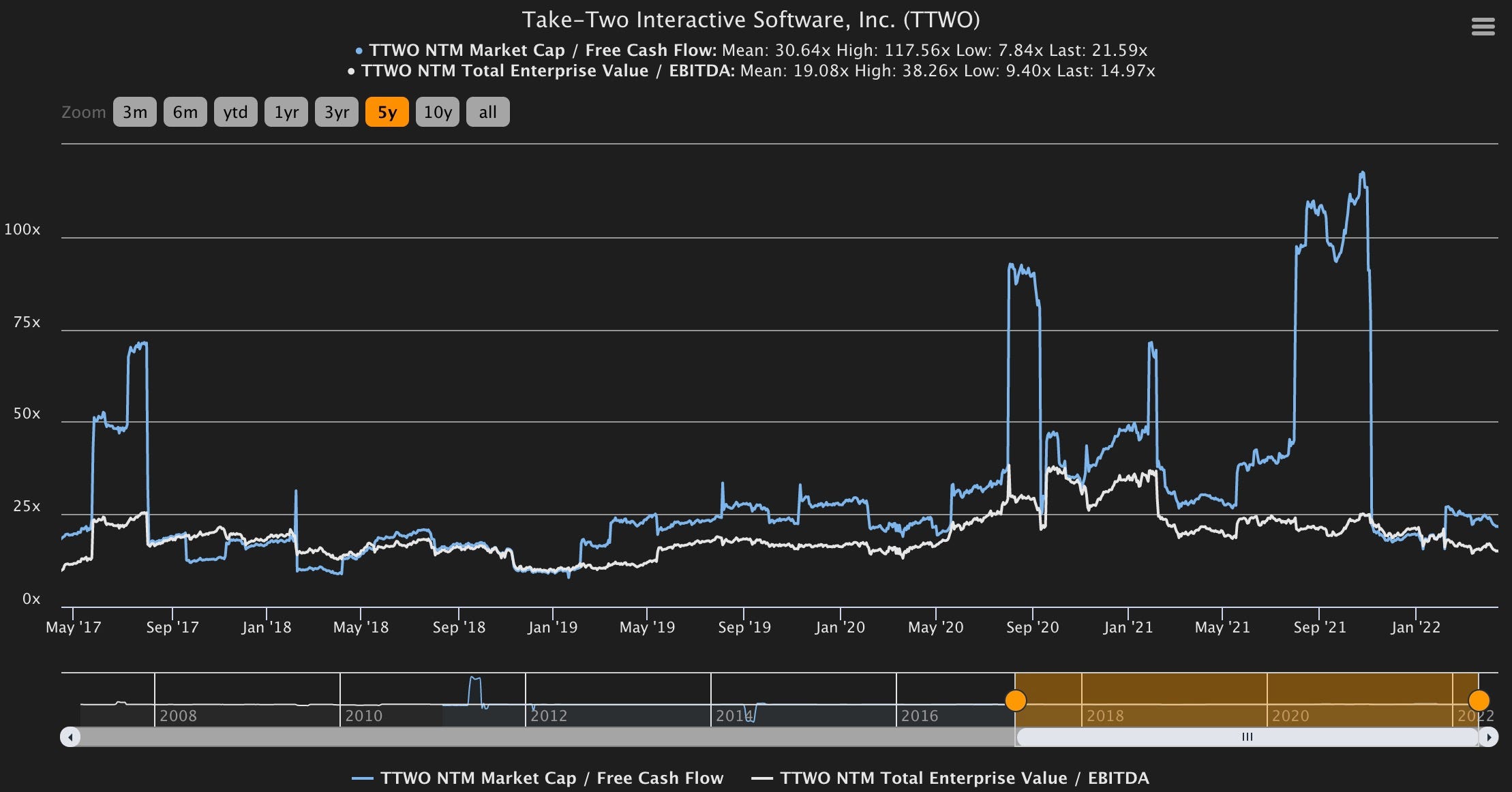

Now, the objective of this section is to find peers with which to establish target multiples for our company. Ubisoft and Take-Two were considered, however, their price multiples show such volatility that they aren’t useful as peers. Here is a sample of what was said:

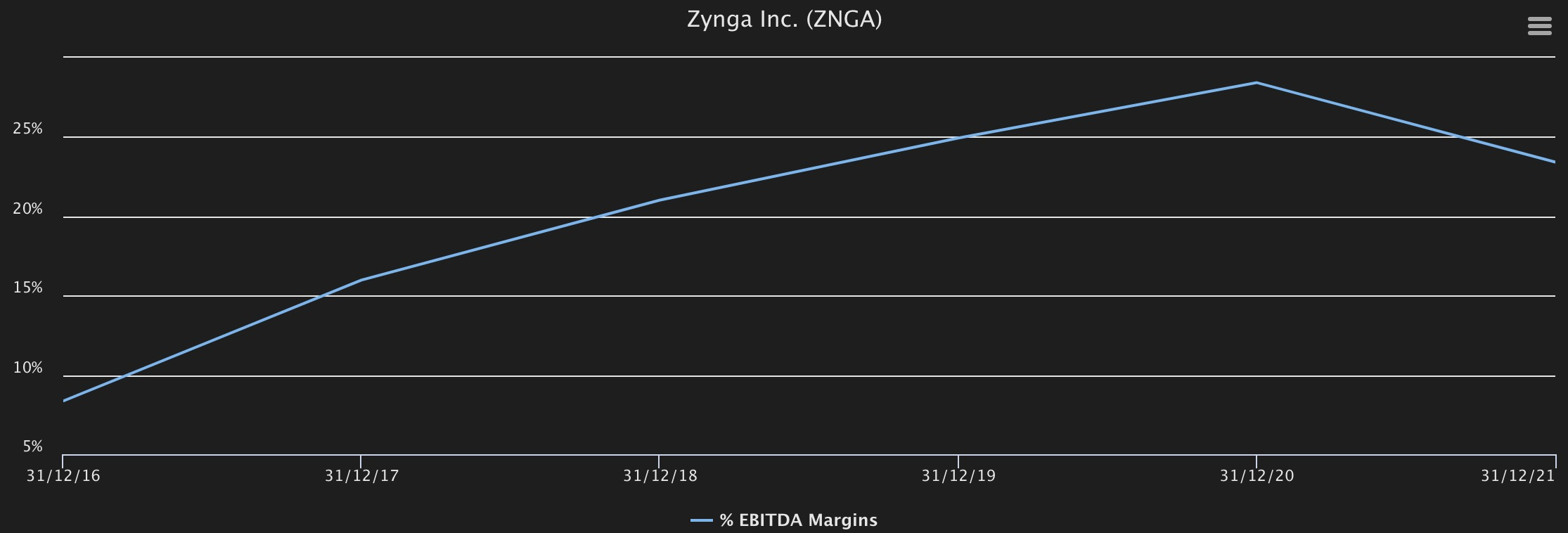

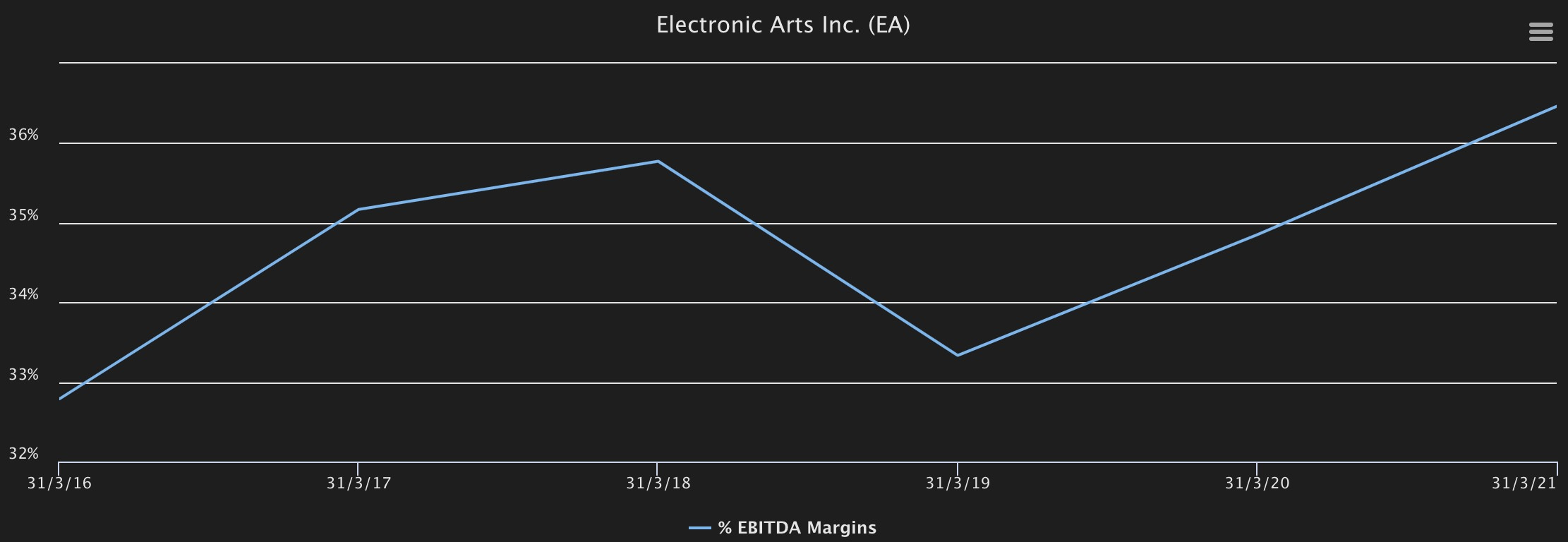

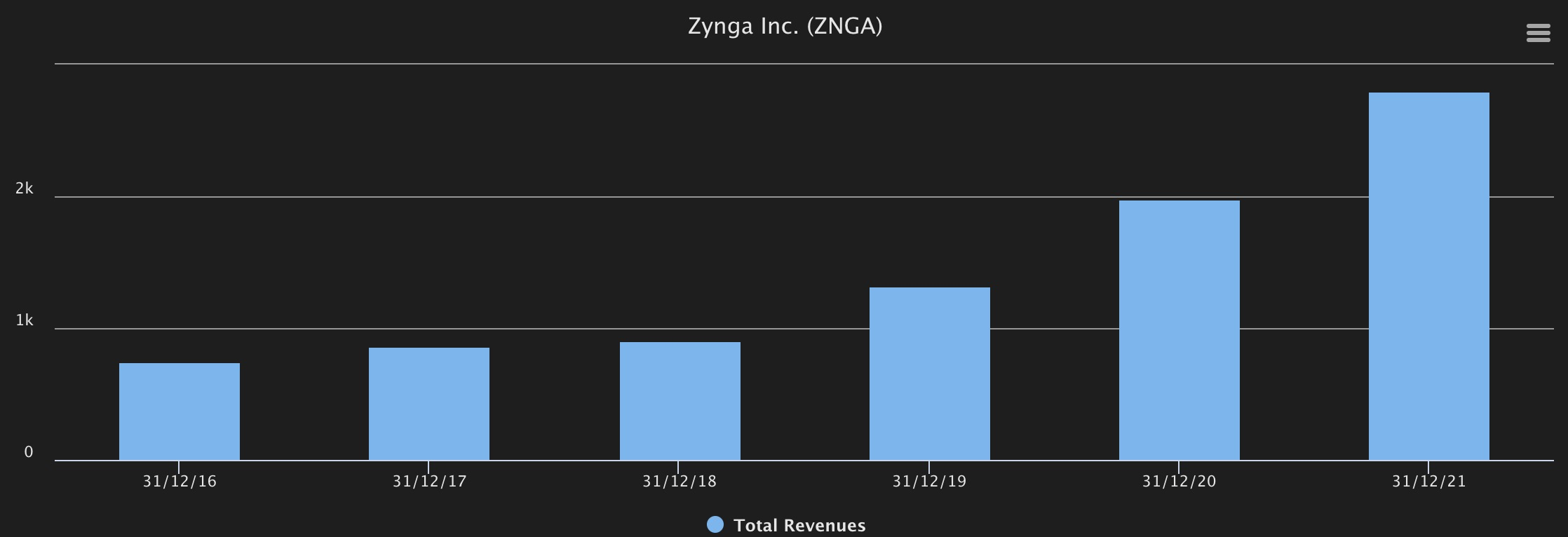

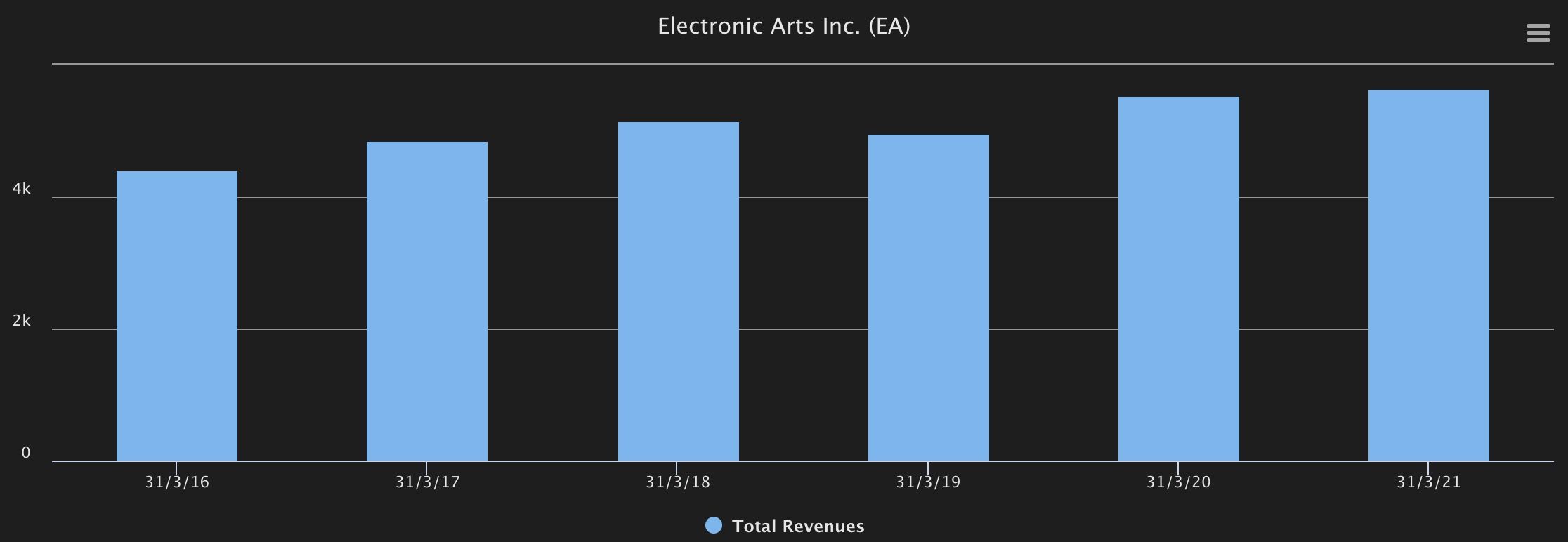

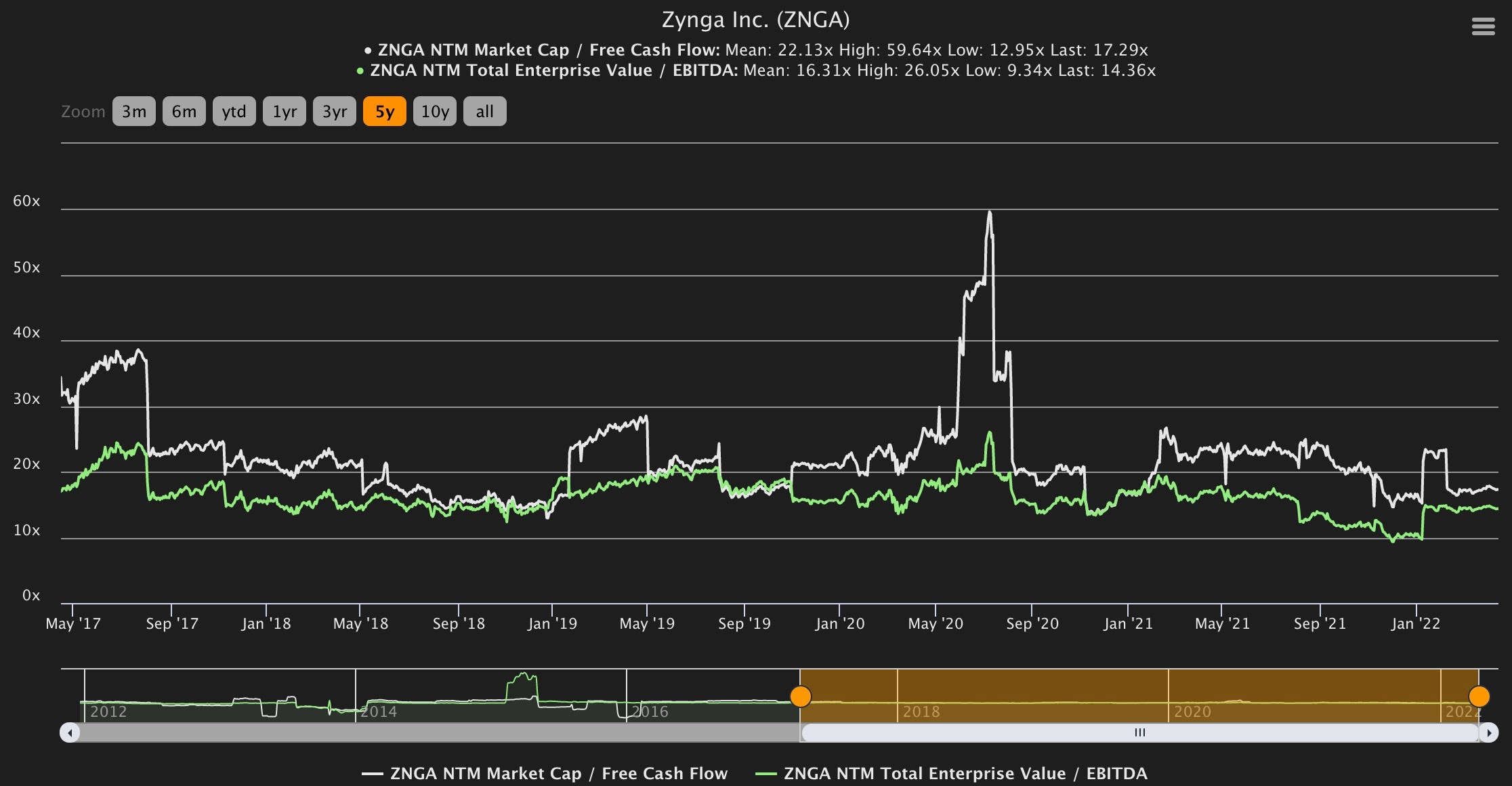

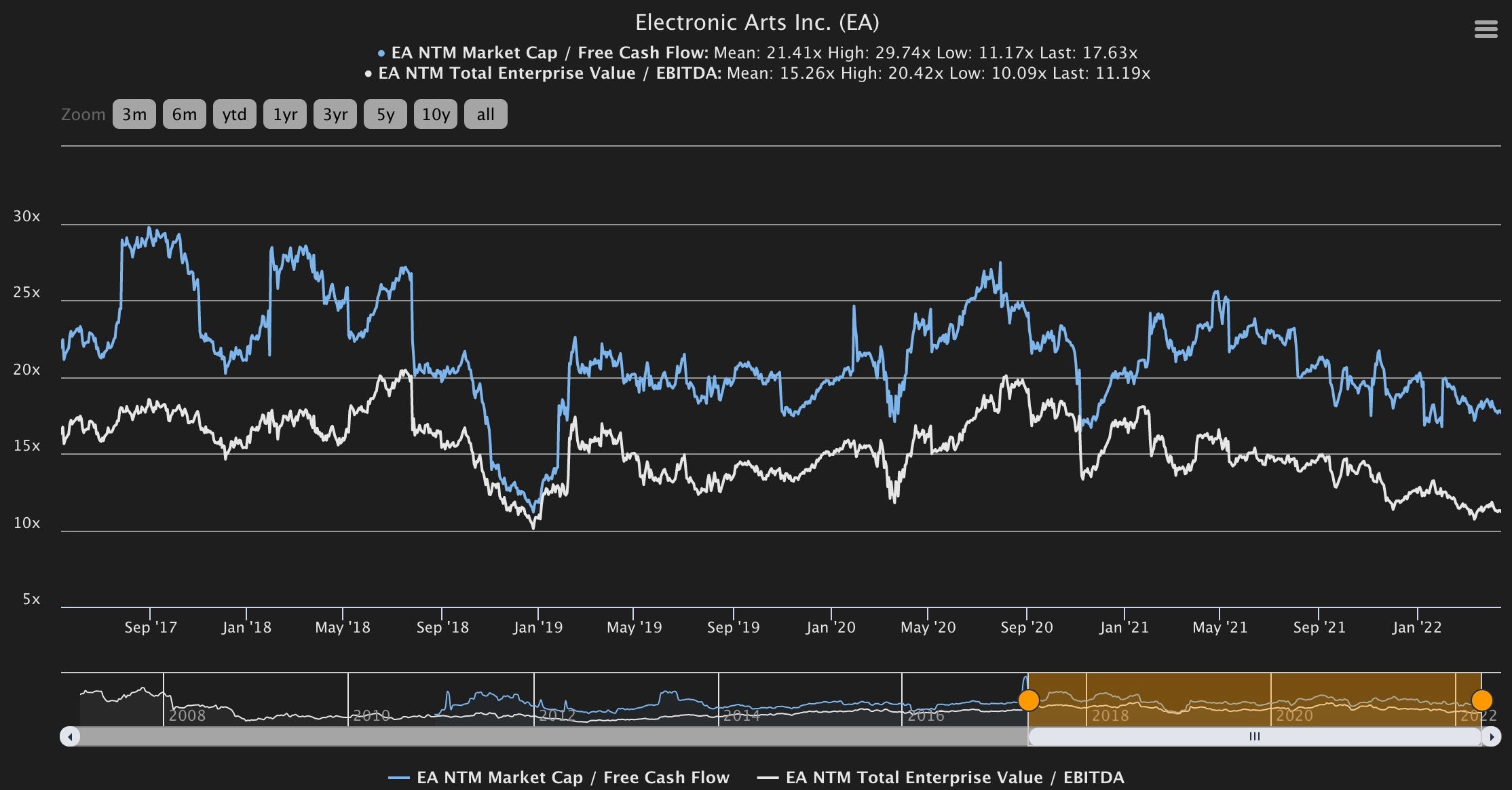

The 2 pairs that have been considered are Zynga and Electronic Arts, both of which are publicly traded companies. Given the natural trend towards acquisitions in the industry, instead of the EBIT Margin, it is more relevant to check the EBITDA Margin:

We observe that the natural trend of both is bullish and Embracer is the company with the best margins, followed by EA and finally Zynga. However, this must be contrasted with sales growth, a sign that there is demand for the company's products.

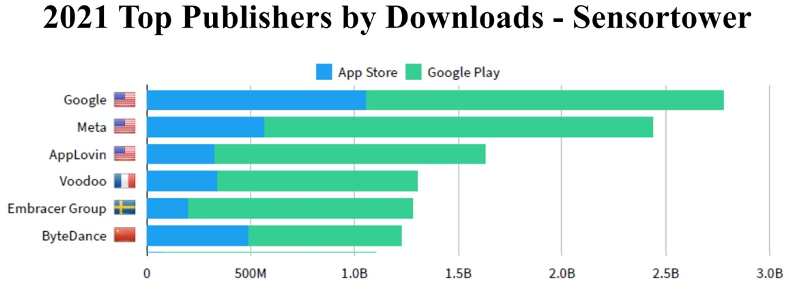

It is clear that the acceleration of sales by Zynga and Embracer is exceptional, and we see this is the hard part for EA. To end this section, let's review which have been the most popular publishers of 2021, according to Sensor Tower:

9. Valuation

Having seen the above, now let's take a look at the multiples of Zynga and Electronic Arts, our company's peers.

The average P/FCF for the last 5 years has been 22x and 21x at Zynga and EA, respectively; while the average EV/EBITDA of the last 5 years has been 16x and 15x in Zynga and EA, respectively. Growth as explosive as that of Embracer is not expected for these two companies.

Now, let's review the EMBRAC data:

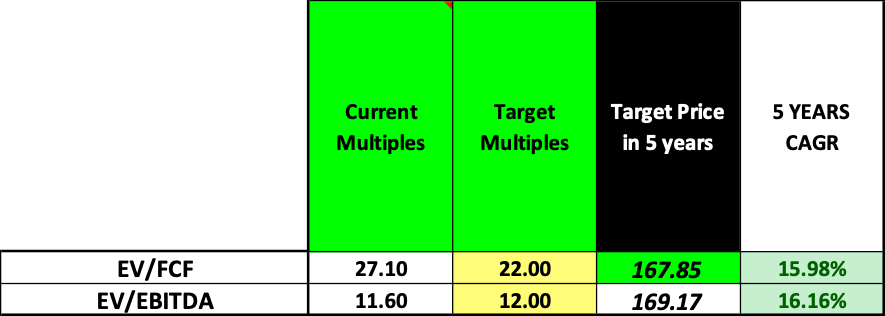

As you can see, we have tried to be very conservative with the valuation. It is worth mentioning that in these projections, a constant annual dilution of 4% has been assumed and we still do not have the FY 2021/2022 annual report, so pessimistic estimates have been made using analyst projections and those offered by EMBRAC itself as a reference. Regarding the EV/FCF (we did not choose P/FCF because, to be conservative, we project net debt and we would be favoring it if we did not take it into account), the calculated 2021 FCF is SEK 2.6B and we project that by 2026 it will be SEK 9.9B. Given the rapid growth we expect, we have chosen the 22x multiple (which could be 25x), since Zynga and EA have the same historical multiple for the last 5 years. All this gives us a price target of SEK 167.85.

In the case of EV/EBITDA, the calculated 2021 EBITDA is SEK 6.1B. and we project that by 2026 it will be SEK 18.3B. It is necessary to mention that the company announced they will be devoting USD 5M to help its employees affected by the war in Ukraine (see here). The use of USD 10M (SEK 100M) for these purposes has been reflected in the projections that we have made of the EBIT (which obviously affects the EBITDA and the aforementioned FCF), but it is a single one-off expense. Despite the rapid growth that we expect, we have chosen the 12x multiple (which could be 15x and even higher). Both Zynga and EA have traded for the last 5 years at a higher multiple. All this gives us a target price of SEK 169.17 in 2026.

To the above, we must add something relevant: Embracer plans to go public on Sweden's main market, the Nasdaq Stockholm Main Market, at the end of 2022. This will undoubtedly be a strong catalyst, since it would put it in the eye of large institutional investors and would give the stock more liquidity and volume, helping to expand the projected multiple. For the latter, debt reduction can also help. For the general knowledge of those interested, in September 2021, EMBRAC had a 2:1 split (see here).

10. Risks

Increased debt that they cannot pay as a result of their acquisition program (in an environment of rampant interest rates, this could be dangerous).

Uncontrollable increase in dilution as a result of its acquisition program (in an environment of contraction of multiples, it could be dangerous).

Risk of conflict in Europe, one of its main markets.

Links of interest:

- CEO interview in English (see here).

- Explanatory video of Embracer (see here).

- Embracer's theses [in English, see here //// in Spanish, see here, a target price is given in the range of SEK 292.2 and SEK 306 (SEK 146.1 and SEK 153 post-split 2:1, close to the target price calculated by me)].

- CEO interview on Spotify (see here).

- Video game conference in Sweden (see here).

- Videos about Embracer in languages other than English (see here, here, here and here).

- EMBRAC letter regarding the war in Ukraine (see here).

- Twitter account with relevant news for Embracer investors (see here).